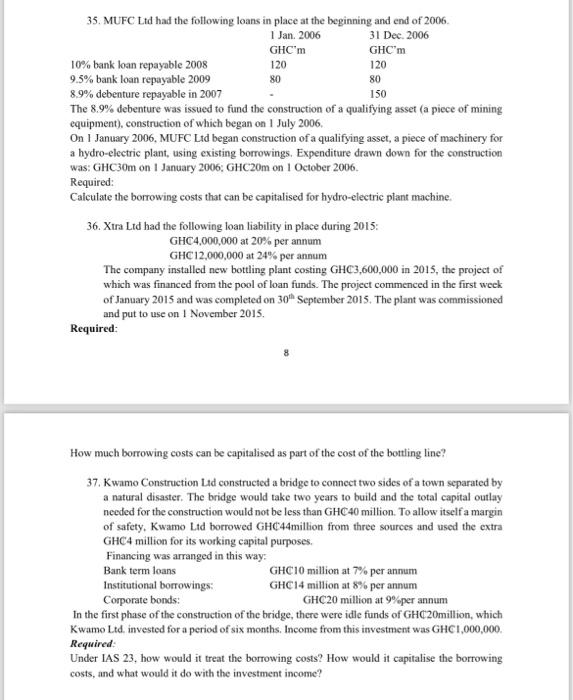

35. MUFC Ltd had the following loans in place at the beginning and end of 2006. ! 1 The 8.9% debenture was issued to fund the construction of a qualifying asset (a piece of mining equipment), construction of which began on 1 July 2006. On I January 2006, MUFC Ltd began construction of a qualifying asset, a piece of machinery for a hydro-electric plant, using existing borrowings. Expenditure drawn down for the construction was: GHC 30m on I January 2006; GHC20m on 1 October 2006. Required: Calculate the borrowing costs that can be capitalised for bydro-electric plant machine. 36. Xtra Ltd had the following loan liability in place during 2015: GHC4,000,000 at 20% per annum GHC12,000,000 at 24% per annum The company installed new bottling plant costing GHC3,600,000 in 2015 , the project of which was financed from the pool of loan funds. The project commenced in the first week of January 2015 and was completed on 30th September 2015. The plant was commissioned and put to use on 1 Nowember 2015. Required: 8 How much borrowing costs can be capitalised as part of the cost of the bottling line? 37. Kwamo Construction Lid constructed a bridge to connect two sides of a town separated by a natural disaster. The bridge would take two years to build and the total capital outlay needed for the construction would not be less than GHC 40 miltion. To allow itself a margin of safety, Kwamo Ltd borrowed GHC44million from three sources and used the extra GHC4 million for its working capital purposes. Financing was arranged in this way: Bank term loans GHC10 million at 7% per annum Institutional borrowings: GHC14 million at 8% per annum Corporate bonds: GHC20 million at 9% per annum In the first phase of the construction of the bridge, there were idle funds of GHC2Omillion, which Kwamo L.d. invested for a period of six months. Income from this investment was GHCl,000,000. Required: Under IAS 23, how would it treat the borrowing costs? How would it capitalise the borrowing costs, and what would it do with the investment income? 38. On 1st January 2015 UNICBET Ltd borrowed GHC6M at 20% interest to finance the construction of a new office building which was expected to take a year (12 months) to complete. Payments to the contractor were made as follows: Idle funds were invested temporarily during 2015, yielding an interest income of GHC200,000. Calculate the borrowing cost to capitalise. 40. Extra Ltd owns a building in Accra which it has been using as a head office. In order to reduce costs, on 30 June 2009 , it moved its head office functions to one of its production centres in Kasoa, and is now letting out its head office. Company policy is to use the fair value model for investment property. 9 The building had an original cost on 1th January 2000 of GHC 250,000 and was being depreciated over 50 years. At 3144 December 2009, its fair value was judged to be GHC 350,000 . How will this appear in the financial statements at 31st December 2009