Answered step by step

Verified Expert Solution

Question

1 Approved Answer

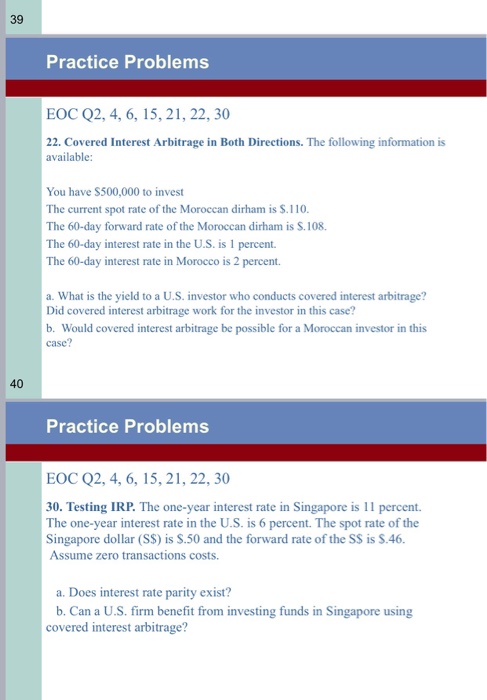

39 Practice Problems EOC Q2, 4, 6, 15, 21, 22, 30 22. Covered nerst Arbitrage in Both Directions. The following information is available: You have

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managing Risk And Uncertainty A Strategic Approach

Authors: Richard Friberg

1st Edition

0262528193,026233156X