Answered step by step

Verified Expert Solution

Question

1 Approved Answer

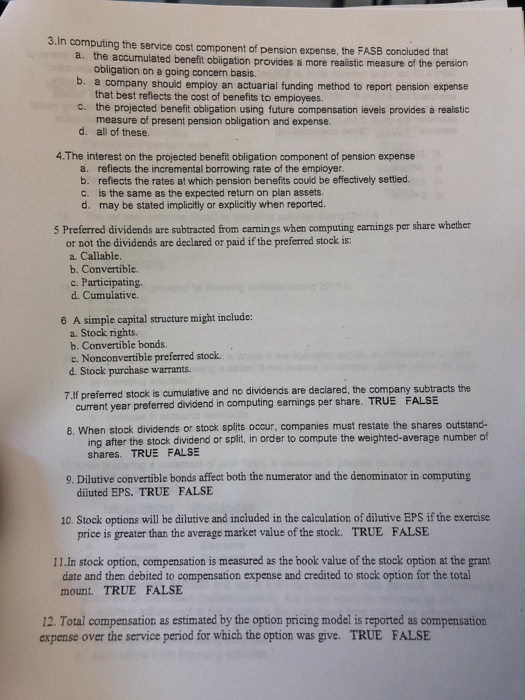

3.In computing the service cost component of pension expense, the FASB concluded that a. the accumulated benefit obligation provides a more realistic b. a company

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ACCA Advanced Audit And Assurance

Authors: Nick Blackwell, Annabel Lefton, Emile Woolf International

1st Edition

1848434715, 978-1848434714