Answered step by step

Verified Expert Solution

Question

1 Approved Answer

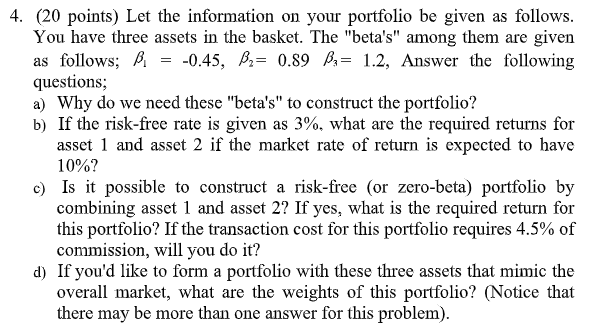

4. (20 points) Let the information on your portfolio be given as follows. You have three assets in the basket. The beta's among them are

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Anthony Saunders, Marcia Cornett

4th Edition

0077262379, 978-0077262372