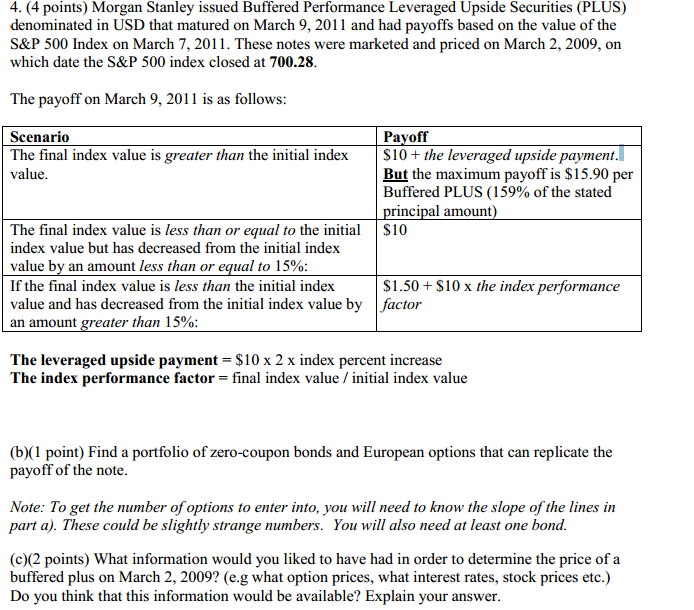

4. (4 points) Morgan Stanley issued Buffered Performance Leveraged Upside Securities (PLUS) denominated in USD that matured on March 9, 2011 and had payoffs based on the value of the S&P 500 Index on March 7, 2011. These notes were marketed and priced on March 2, 2009, on which date the S&P 500 index closed at 700.28. The payoff on March 9, 2011 is as follows: Scenario Payoff The final index value is greater than the initial index value. $ 10 + the leveraged upside payment. But the maximum payoff is $15.90 per Buffered PLUS (159% of the stated principal amount) The final index value is less than or equal to the initial index value but has decreased from the initial index value by an amount less than or equal to 15%: $ 10 If the final index value is less than the initial index value and has decreased from the initial index value by an amount greater than 15%: $ 1.50 + $ 10 x the index performance factor The leveraged upside payment = $10 x 2 x index percent increase The index performance factor = final index value /initial index value (b)(1 point) Find a portfolio of zero-coupon bonds and European options that can replicate the payoff of the note. Note: To get the number of options to enter into, you will need to know the slope of the lines in part a). These could he slightly strange numbers. You will also need at least one bond. (c)(2 points) What information would you liked to have had in order to determine the price of a buffered plus on March 2, 2009? (e.g what option prices, what interest rates, stock prices etc.) Do you think that this information would be available? Explain your answer. 4. (4 points) Morgan Stanley issued Buffered Performance Leveraged Upside Securities (PLUS) denominated in USD that matured on March 9, 2011 and had payoffs based on the value of the S&P 500 Index on March 7, 2011. These notes were marketed and priced on March 2, 2009, on which date the S&P 500 index closed at 700.28. The payoff on March 9, 2011 is as follows: Scenario Payoff The final index value is greater than the initial index value. $ 10 + the leveraged upside payment. But the maximum payoff is $15.90 per Buffered PLUS (159% of the stated principal amount) The final index value is less than or equal to the initial index value but has decreased from the initial index value by an amount less than or equal to 15%: $ 10 If the final index value is less than the initial index value and has decreased from the initial index value by an amount greater than 15%: $ 1.50 + $ 10 x the index performance factor The leveraged upside payment = $10 x 2 x index percent increase The index performance factor = final index value /initial index value (b)(1 point) Find a portfolio of zero-coupon bonds and European options that can replicate the payoff of the note. Note: To get the number of options to enter into, you will need to know the slope of the lines in part a). These could he slightly strange numbers. You will also need at least one bond. (c)(2 points) What information would you liked to have had in order to determine the price of a buffered plus on March 2, 2009? (e.g what option prices, what interest rates, stock prices etc.) Do you think that this information would be available? Explain your