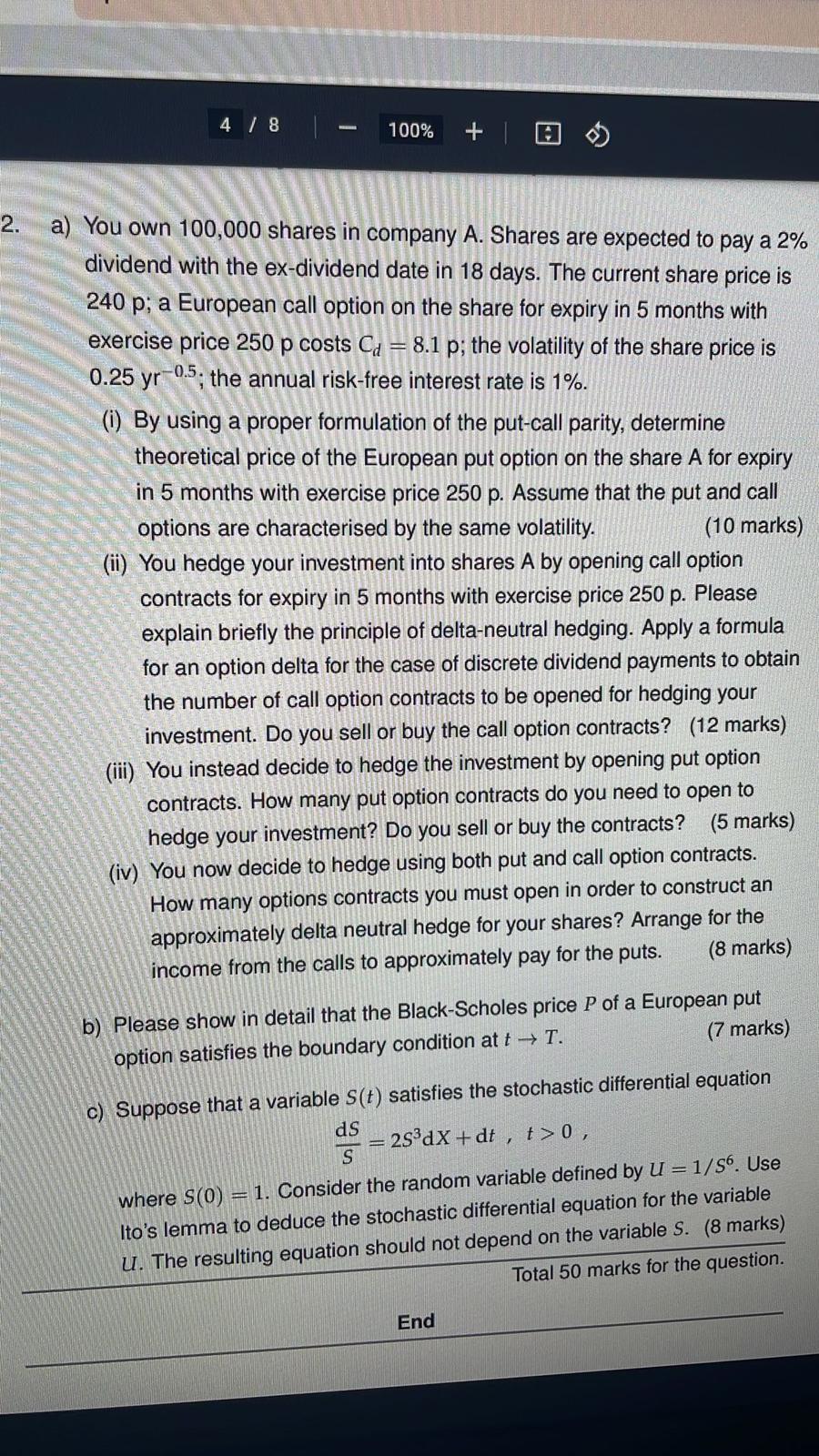

4 / 8 100% + = 2. a) You own 100,000 shares in company A. Shares are expected to pay a 2% dividend with the ex-dividend date in 18 days. The current share price is 240 p; a European call option on the share for expiry in 5 months with exercise price 250 p costs Cd = 8.1 p; the volatility of the share price is 0.25 yr-0.5, the annual risk-free interest rate is 1%. (i) By using a proper formulation of the put-call parity, determine theoretical price of the European put option on the share A for expiry in 5 months with exercise price 250 p. Assume that the put and call options are characterised by the same volatility. (10 marks) (ii) You hedge your investment into shares A by opening call option contracts for expiry in 5 months with exercise price 250 p. Please explain briefly the principle of delta-neutral hedging. Apply a formula for an option delta for the case of discrete dividend payments to obtain the number of call option contracts to be opened for hedging your investment. Do you sell or buy the call option contracts? (12 marks) (iii) You instead decide to hedge the investment by opening put option contracts. How many put option contracts do you need to open to hedge your investment? Do you sell or buy the contracts? (5 marks) (iv) You now decide to hedge using both put and call option contracts. How many options contracts you must open in order to construct an approximately delta neutral hedge for your shares? Arrange for the (8 marks) income from the calls to approximately pay for the puts. b) Please show in detail that the Black-Scholes price P of a European put option satisfies the boundary condition at t T. (7 marks) 7 c) Suppose that a variable S(t) satisfies the stochastic differential equation ds 283X + dt t>O, S where S(0) = 1. Consider the random variable defined by U = 1/36. Use Ito's lemma to deduce the stochastic differential equation for the variable u. The resulting equation should not depend on the variable S. (8 marks) Total 50 marks for the question. End 4 / 8 100% + = 2. a) You own 100,000 shares in company A. Shares are expected to pay a 2% dividend with the ex-dividend date in 18 days. The current share price is 240 p; a European call option on the share for expiry in 5 months with exercise price 250 p costs Cd = 8.1 p; the volatility of the share price is 0.25 yr-0.5, the annual risk-free interest rate is 1%. (i) By using a proper formulation of the put-call parity, determine theoretical price of the European put option on the share A for expiry in 5 months with exercise price 250 p. Assume that the put and call options are characterised by the same volatility. (10 marks) (ii) You hedge your investment into shares A by opening call option contracts for expiry in 5 months with exercise price 250 p. Please explain briefly the principle of delta-neutral hedging. Apply a formula for an option delta for the case of discrete dividend payments to obtain the number of call option contracts to be opened for hedging your investment. Do you sell or buy the call option contracts? (12 marks) (iii) You instead decide to hedge the investment by opening put option contracts. How many put option contracts do you need to open to hedge your investment? Do you sell or buy the contracts? (5 marks) (iv) You now decide to hedge using both put and call option contracts. How many options contracts you must open in order to construct an approximately delta neutral hedge for your shares? Arrange for the (8 marks) income from the calls to approximately pay for the puts. b) Please show in detail that the Black-Scholes price P of a European put option satisfies the boundary condition at t T. (7 marks) 7 c) Suppose that a variable S(t) satisfies the stochastic differential equation ds 283X + dt t>O, S where S(0) = 1. Consider the random variable defined by U = 1/36. Use Ito's lemma to deduce the stochastic differential equation for the variable u. The resulting equation should not depend on the variable S. (8 marks) Total 50 marks for the question. End