Answered step by step

Verified Expert Solution

Question

1 Approved Answer

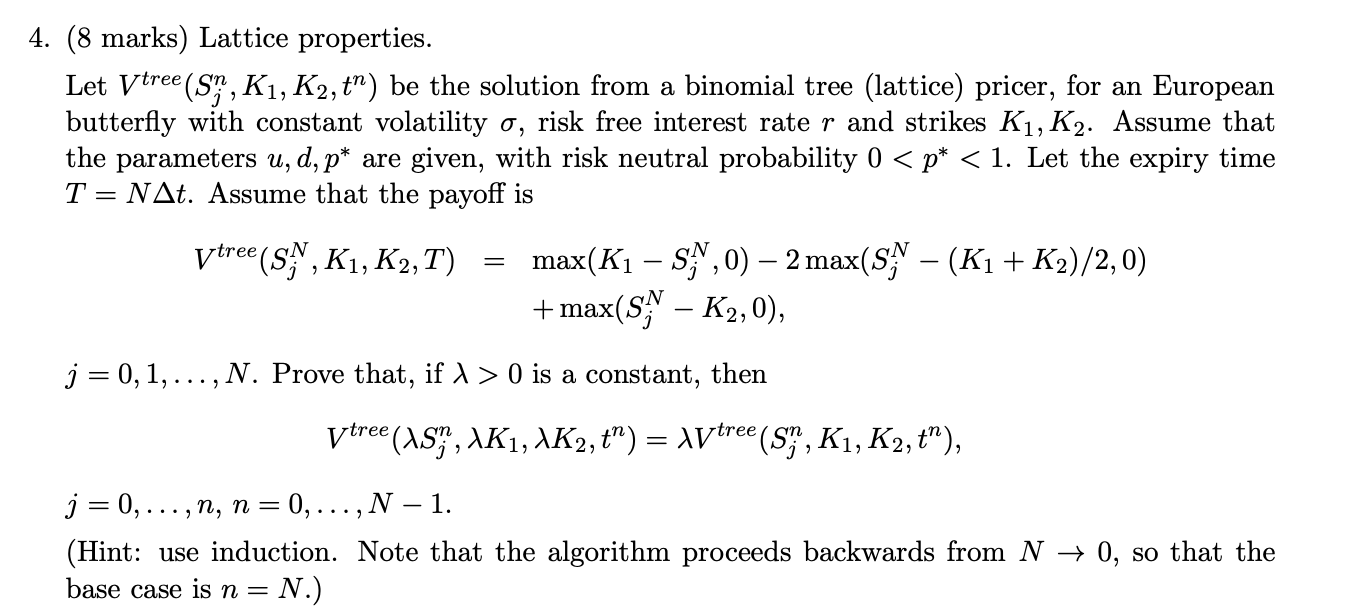

4. (8 marks) Lattice properties. Let ytree (S, K1, K2, t) be the solution from a binomial tree (lattice) pricer, for an European butterfly with

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Scientific And Statistical Database Management 2 International Conference Ssdbm 2012 Chania Crete Greece June 2012 Proceedings Lncs 7338

Authors: Anastasia Ailamaki ,Shawn Bowers

2012 Edition

3642312349, 978-3642312342