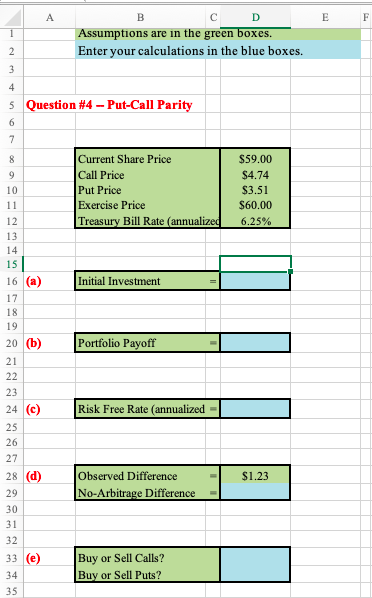

4. A share of ABC Corp. is currently trading at $59 per share. European call and put options are available with an exercise price of $60 at a price of $4.74 and $3.51, respectively. They can be exercised in exactly six months. The current xix-month Treasury bill rate (annualized) is 6.25%. ABC Corp. does not currently pay dividends. Suppose that you purchase one share of stock and one put option. You also sell one call option (a) What is your total initial investment? (b) What will be the payoff of this portfolio in six months? (C) What is the annualized risk-free rate of return for this portfolio? (d) Notice the observed difference between the call price and put price is $1.23. Calculate the "no-arbitrage difference that would exist in an efficient market, given the current risk-free interest rate? (e) Would investors buy or sell call options in order to take advantage of an arbitrage opportunity? Would investors buy or sell put options? A D E F 1 B Assumptions are in the green boxes. Enter your calculations in the blue boxes. 2 3 4 5 Question #4 - Put-Call Parity 6 7 8 Current Share Price Call Price Put Price Exercise Price Treasury Bill Rate (annualized $59.00 $4.74 $3.51 $60.00 6.25% Initial Investment Portfolio Payoff 9 10 11 12 13 14 15 16 (a) 17 18 19 20 (b) 21 22 23 24 ) 25 26 27 28 (d) 29 30 31 32 33 (e) 34 35 Risk Free Rate (annualized $1.23 Observed Difference No-Arbitrage Difference Buy or Sell Calls? Buy or Sell Puts? 4. A share of ABC Corp. is currently trading at $59 per share. European call and put options are available with an exercise price of $60 at a price of $4.74 and $3.51, respectively. They can be exercised in exactly six months. The current xix-month Treasury bill rate (annualized) is 6.25%. ABC Corp. does not currently pay dividends. Suppose that you purchase one share of stock and one put option. You also sell one call option (a) What is your total initial investment? (b) What will be the payoff of this portfolio in six months? (C) What is the annualized risk-free rate of return for this portfolio? (d) Notice the observed difference between the call price and put price is $1.23. Calculate the "no-arbitrage difference that would exist in an efficient market, given the current risk-free interest rate? (e) Would investors buy or sell call options in order to take advantage of an arbitrage opportunity? Would investors buy or sell put options? A D E F 1 B Assumptions are in the green boxes. Enter your calculations in the blue boxes. 2 3 4 5 Question #4 - Put-Call Parity 6 7 8 Current Share Price Call Price Put Price Exercise Price Treasury Bill Rate (annualized $59.00 $4.74 $3.51 $60.00 6.25% Initial Investment Portfolio Payoff 9 10 11 12 13 14 15 16 (a) 17 18 19 20 (b) 21 22 23 24 ) 25 26 27 28 (d) 29 30 31 32 33 (e) 34 35 Risk Free Rate (annualized $1.23 Observed Difference No-Arbitrage Difference Buy or Sell Calls? Buy or Sell Puts