Answered step by step

Verified Expert Solution

Question

1 Approved Answer

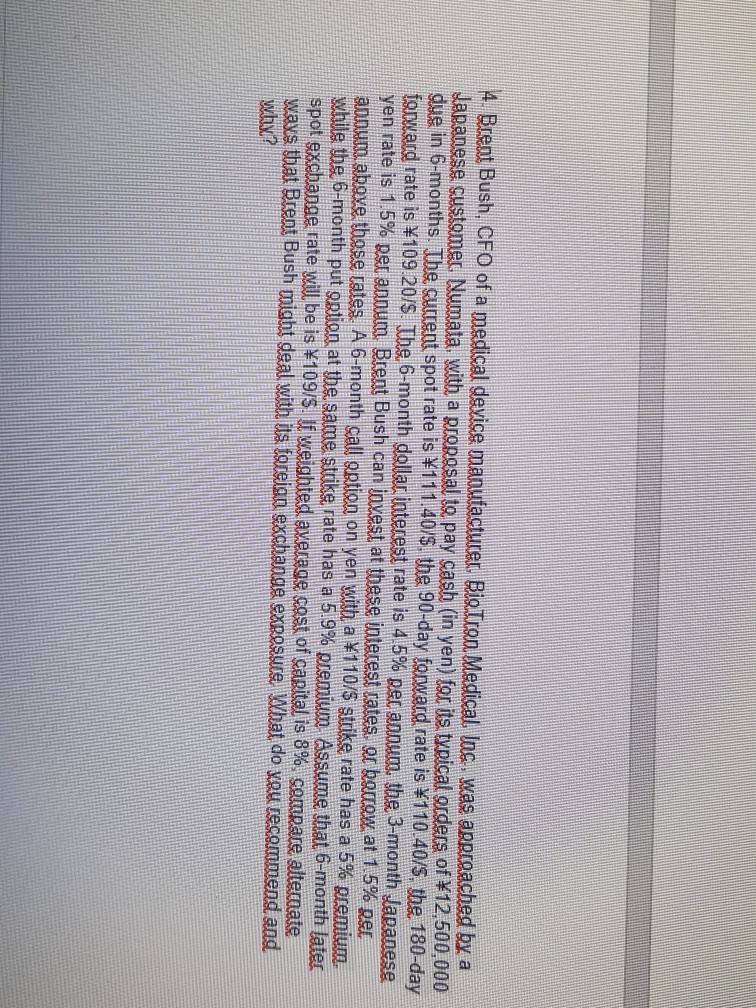

4. Brent Bush, CFO of a medical device manufacturer. Ristian Medical Jos was approached by a Japanese customer, Numata, with a proposal to pay sash

4. Brent Bush, CFO of a medical device manufacturer. Ristian Medical Jos was approached by a Japanese customer, Numata, with a proposal to pay sash (in yen) for its typical orders of #12,500,000 due in 6-months. The curent spot rate is 111.40/$. the 90-day forward rate is $110.40/5, the 180-day forward rate is 109.20/S. The 6-month dollar interest rate is 4.5% Rec annum, the 3-month Japanese yen rate is 1.5% per annum Brent Bush can javest at these interest rates, er betrow, at 1.5% ner abym above those rates. A 6-month call option on yen with a 110/$ strike rate has a 5% premium. while the 6-month put option at the same strike rate has a 5.9% premium Assume that 6-month later spot exchange rate will be is 10975. U weighted average cost of capital is 8%, semnare alternate ways that Brent Bush might deal with its foreign exchange exposure What do you recommend and whx

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Public Finance Lessons From The Past And Effects On The Future

Authors: Miguel-Angel Galindo Martin

1st Edition

1629481491, 978-1629481494