Question

4. To achieve international diversification, John invests in the USA and India indexes. What are the weights on the two indexes to achieve the optimal

4. To achieve international diversification, John invests in the USA and India indexes. What are the weights on the two indexes to achieve the optimal international portfolio? What are the mean and standard deviation of returns on his optimal international portfolio?

4. To achieve international diversification, John invests in the USA and India indexes. What are the weights on the two indexes to achieve the optimal international portfolio? What are the mean and standard deviation of returns on his optimal international portfolio?

please show me steps on excel how they compute this on excel, check pic which I upload.

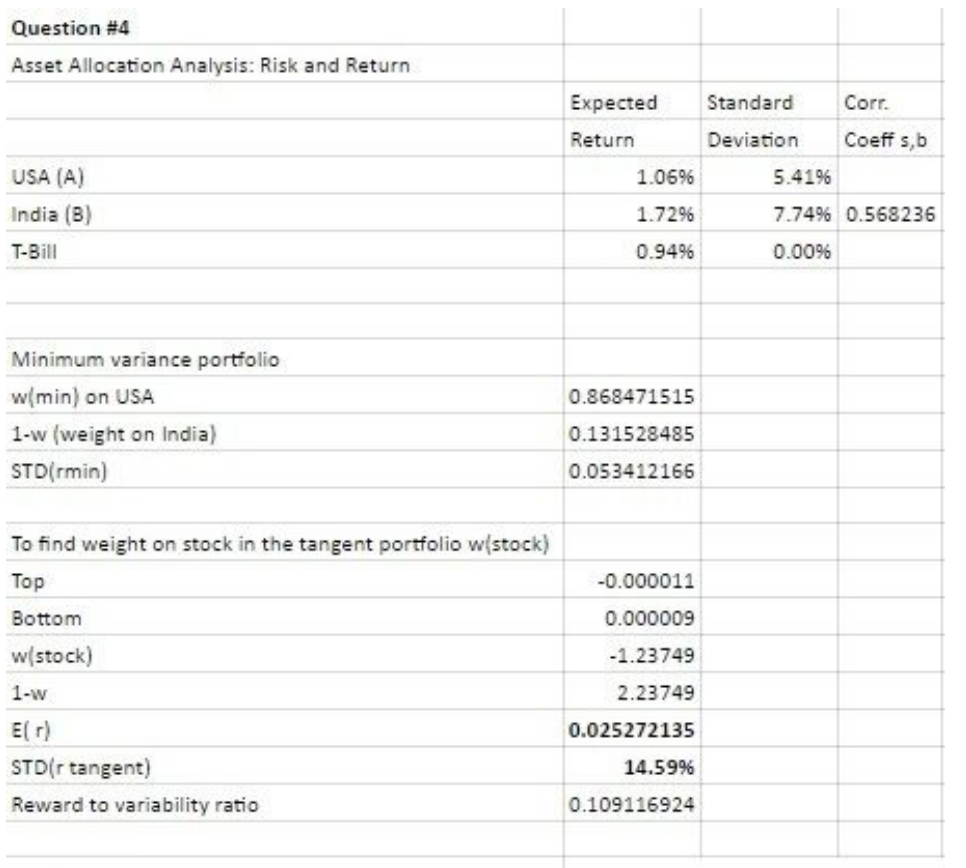

Question #4 Asset Allocation Analysis: Risk and Return Expected Standard Corr. Deviation Coeff s,b Return USA (A) 1.0696 5.41% India (B) 1.7296 7.7496 0.568236 0.0096 0.94% Minimum variance portfolio w(min) on USA 0.868471515 1-w (weight on India) 0.131528485 STO(rmin) 0.053412166 To find weight on stock in the tangent portfolio wistock) Top -0.000011 0.000009 Bottom w(stock -1.23749 1-w 2.23749 0.025272135 (r) STD(r tangent) 14.599% Reward to variability ratio 0.109116924Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of The Political Economy Of Financial Crises

Authors: Martin H. Wolfson, Gerald A. Epstein

1st Edition

0199757232, 978-0199757237