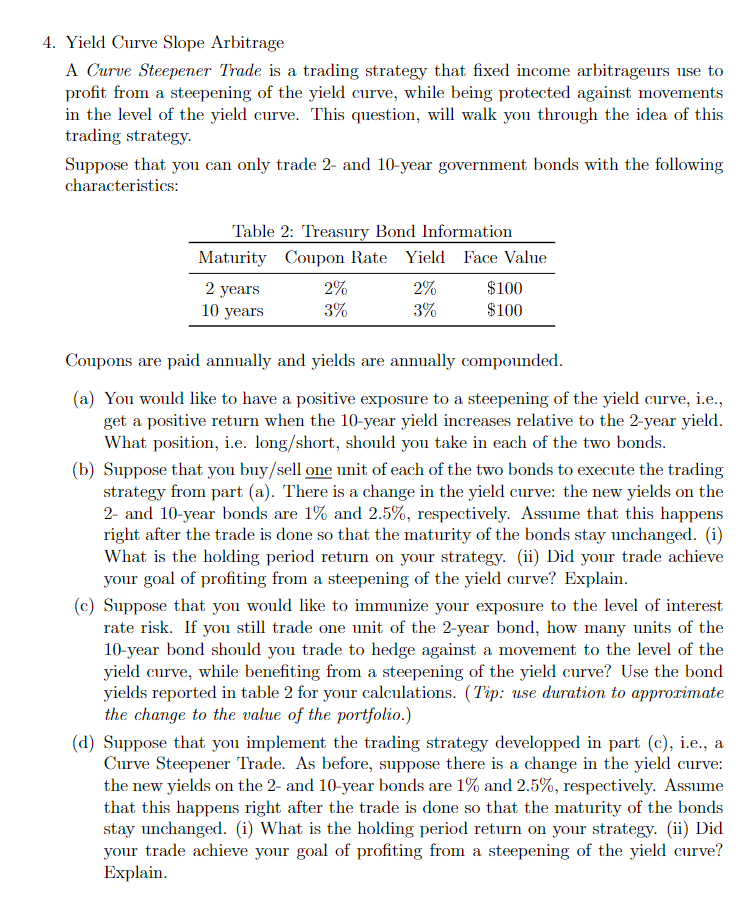

4. Yield Curve Slope Arbitrage A Curve Steepener Trade is a trading strategy that fixed income arbitrageurs use to profit from a steepening of the yield curve, while being protected against movements in the level of the yield curve. This question, will walk you through the idea of this trading strategy. Suppose that you can only trade 2- and 10-year government bonds with the following characteristics: Coupons are paid annually and yields are annually compounded. (a) You would like to have a positive exposure to a steepening of the yield curve, i.e., get a positive return when the 10-year yield increases relative to the 2-year yield. What position, i.e. long/short, should you take in each of the two bonds. (b) Suppose that you buy/sell one unit of each of the two bonds to execute the trading strategy from part (a). There is a change in the yield curve: the new yields on the 2- and 10-year bonds are 1% and 2.5%, respectively. Assume that this happens right after the trade is done so that the maturity of the bonds stay unchanged. (i) What is the holding period return on your strategy. (ii) Did your trade achieve your goal of profiting from a steepening of the yield curve? Explain. (c) Suppose that you would like to immunize your exposure to the level of interest rate risk. If you still trade one unit of the 2-year bond, how many units of the 10-year bond should you trade to hedge against a movement to the level of the yield curve, while benefiting from a steepening of the yield curve? Use the bond yields reported in table 2 for your calculations. (Tip: use duration to approximate the change to the value of the portfolio.) (d) Suppose that you implement the trading strategy developped in part (c), i.e., a Curve Steepener Trade. As before, suppose there is a change in the yield curve: the new yields on the 2- and 10-year bonds are 1% and 2.5%, respectively. Assume that this happens right after the trade is done so that the maturity of the bonds stay unchanged. (i) What is the holding period return on your strategy. (ii) Did your trade achieve your goal of profiting from a steepening of the yield curve? Explain. 4. Yield Curve Slope Arbitrage A Curve Steepener Trade is a trading strategy that fixed income arbitrageurs use to profit from a steepening of the yield curve, while being protected against movements in the level of the yield curve. This question, will walk you through the idea of this trading strategy. Suppose that you can only trade 2- and 10-year government bonds with the following characteristics: Coupons are paid annually and yields are annually compounded. (a) You would like to have a positive exposure to a steepening of the yield curve, i.e., get a positive return when the 10-year yield increases relative to the 2-year yield. What position, i.e. long/short, should you take in each of the two bonds. (b) Suppose that you buy/sell one unit of each of the two bonds to execute the trading strategy from part (a). There is a change in the yield curve: the new yields on the 2- and 10-year bonds are 1% and 2.5%, respectively. Assume that this happens right after the trade is done so that the maturity of the bonds stay unchanged. (i) What is the holding period return on your strategy. (ii) Did your trade achieve your goal of profiting from a steepening of the yield curve? Explain. (c) Suppose that you would like to immunize your exposure to the level of interest rate risk. If you still trade one unit of the 2-year bond, how many units of the 10-year bond should you trade to hedge against a movement to the level of the yield curve, while benefiting from a steepening of the yield curve? Use the bond yields reported in table 2 for your calculations. (Tip: use duration to approximate the change to the value of the portfolio.) (d) Suppose that you implement the trading strategy developped in part (c), i.e., a Curve Steepener Trade. As before, suppose there is a change in the yield curve: the new yields on the 2- and 10-year bonds are 1% and 2.5%, respectively. Assume that this happens right after the trade is done so that the maturity of the bonds stay unchanged. (i) What is the holding period return on your strategy. (ii) Did your trade achieve your goal of profiting from a steepening of the yield curve? Explain