Question

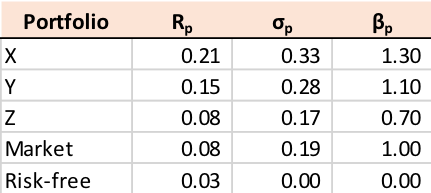

4) You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: What is the Sharpe ratio, Treynor ratio, and

4) You are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: What is the Sharpe ratio, Treynor ratio, and Jensen's alpha for each portfolio (including the market portfolio)?

5) A stock has an annual return of 11 percent and a standard deviation of 49 percent. Assuming returns are normally distributed, what is the smallest expected loss over the next year with a probability of 1 percent? Does this number make sense? Why or why not?

Portfolio 0.21 0.15 0.08 0.08 0.03 0.33 0.28 0.17 0.19 0.00 1.30 1.10 0.70 1.00 0.00 Market Risk-free Portfolio 0.21 0.15 0.08 0.08 0.03 0.33 0.28 0.17 0.19 0.00 1.30 1.10 0.70 1.00 0.00 Market Risk-freeStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Markets And Institutions

Authors: Frederic S. Mishkin, Stanley G. Eakins

7th Edition

013213683X, 978-0132136839