Answered step by step

Verified Expert Solution

Question

1 Approved Answer

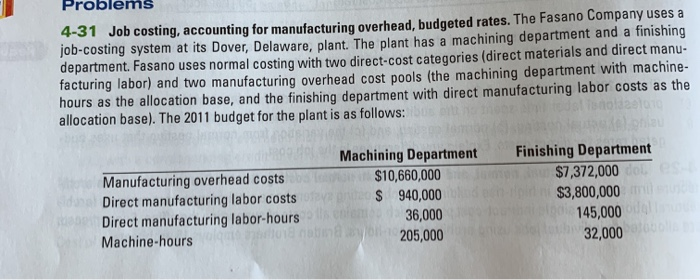

4-29 Job costing; actual, normal, and variation from normal costing. Braden Brothers, Inc., is an archi- tecture firm specializing in high-rise buildings. Its job-costing system

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Energy Audit And Survey Of Street Light System A Preliminary Report

Authors: Dr. Manoj Dhondiram Patil

1st Edition

B08GBCWWFY, 979-8676818388