Answered step by step

Verified Expert Solution

Question

1 Approved Answer

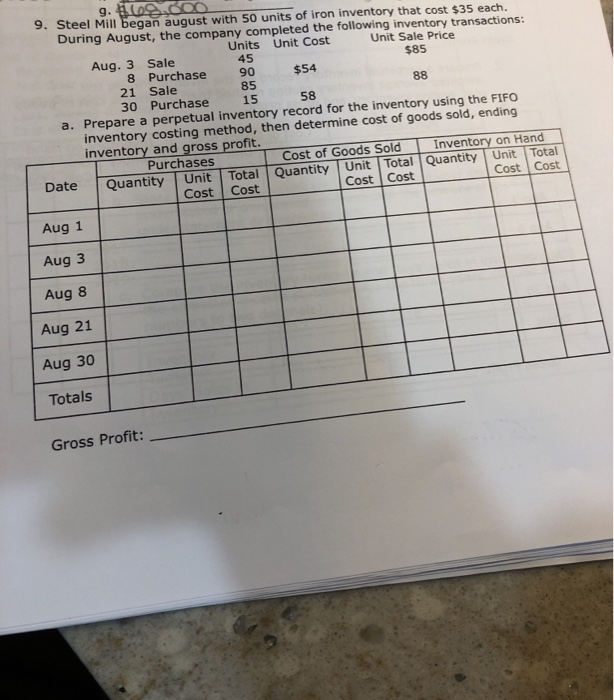

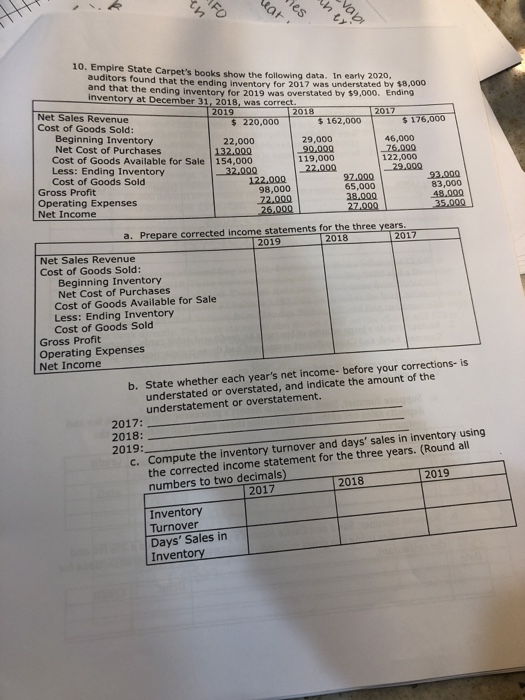

45 85 g. L C00 9. Steel Mill began august with 50 units of iron inventory that cost $35 each. During August, the company completed

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Importance Of An Audit In The Internal Control System Evaluation Of The Internal Control System For Inventory Management In A Commercial Company

Authors: Gabriela Saltos, Hernán Maldonado

1st Edition

6202823798, 978-6202823791