Answered step by step

Verified Expert Solution

Question

1 Approved Answer

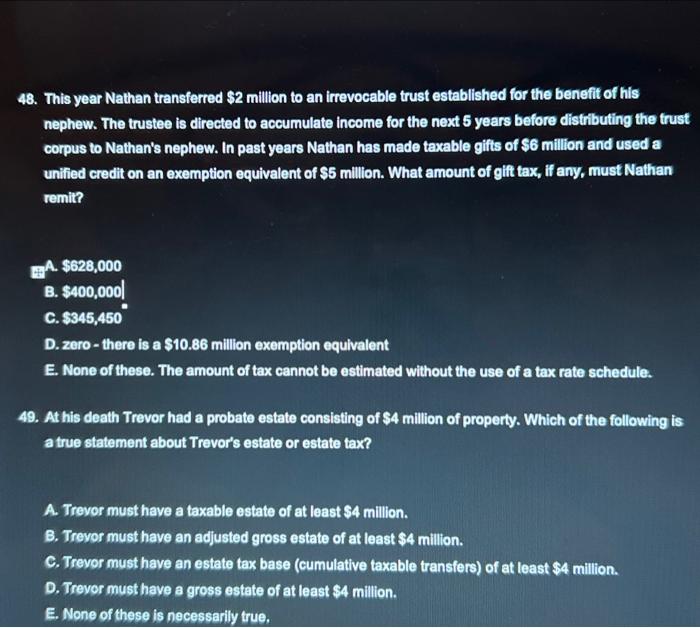

48. This year Nathan transferred $2 million to an irrevocable trust established for the benefit of his nephew. The trustee is directed to accumulate income

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Internal Auditing Assurance And Consulting Services

Authors: Kurt F. Reding, Paul J. Sobel, Urton L. Anderson, Michael J. Head, Sridhar Ramamoorti, Mark Salamasick, Contributing Writer, Cris Ridd, Richard Tuschman

1st Edition

0894136100, 978-0894136108