Answered step by step

Verified Expert Solution

Question

1 Approved Answer

4.8.2 What is the relationship between portfolio VaR and the individual asset VaRs? Is portfolio VaR a weighted average of the individual asset VaRs? 4.8.3

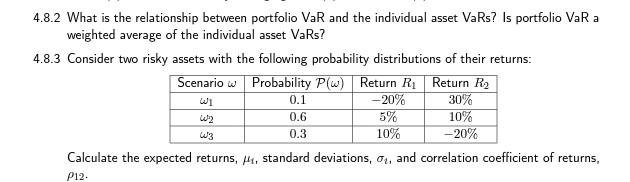

4.8.2 What is the relationship between portfolio VaR and the individual asset VaRs? Is portfolio VaR a weighted average of the individual asset VaRs? 4.8.3 Consider two risky assets with the following probability distributions of their returns: Scenario w Probability P(w) Return R Return R2 -20% 30% 5% 10% 10% -20% Calculate the expected returns, He, standard deviations, 01, and correlation coefficient of returns, 0.1 0.6 0.3 P12

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Management Concepts and Applications

Authors: Stephen Foerster

1st edition

013293664X, 978-0132936644