Answered step by step

Verified Expert Solution

Question

1 Approved Answer

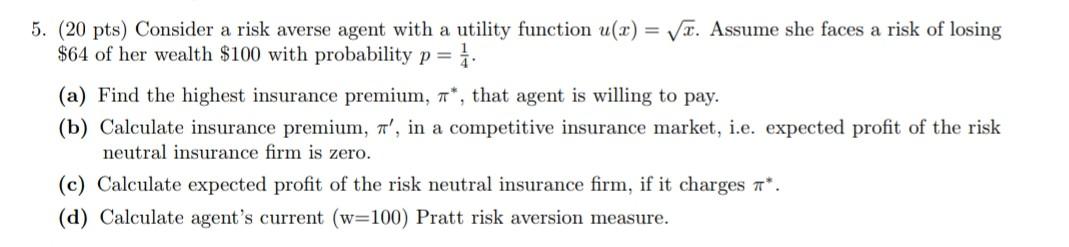

5. (20 pts) Consider a risk averse agent with a utility function u(2) Vx. Assume she faces a risk of losing $64 of her wealth

5. (20 pts) Consider a risk averse agent with a utility function u(2) Vx. Assume she faces a risk of losing $64 of her wealth $100 with probability p= 1. (a) Find the highest insurance premium, 7*, that agent is willing to pay. (b) Calculate insurance premium, 7', in a competitive insurance market, i.e. expected profit of the risk neutral insurance firm is zero. (c) Calculate expected profit of the risk neutral insurance firm, if it charges *. (d) Calculate agent's current (w=100) Pratt risk aversion measure

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Lectures On Urban Economics

Authors: Jan K Brueckner

1st Edition

0262300311, 9780262300315