Question

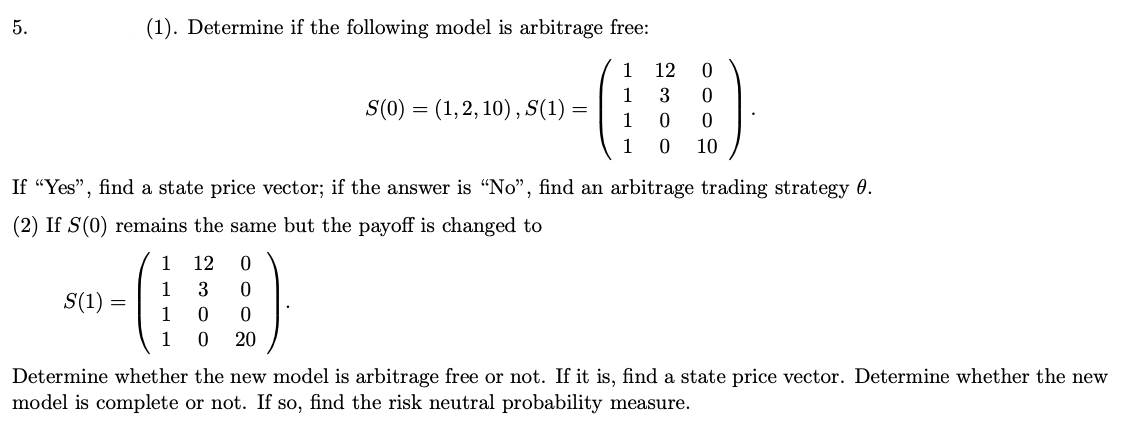

5. (a). Determine if the following model is arbitrage free: 1 12 0 S(0)=(1,2,10),S(1)= 1 3 0 . 1 0 0 1 0 10 If

5. (a). Determine if the following model is arbitrage free: 1 12 0

S(0)=(1,2,10),S(1)= 1 3 0 . 1 0 0

1 0 10 If Yes, find a state price vector; if the answer is No, find an arbitrage trading strategy .

(b) If S(0) remains the same but the payoff is changed to 1 12 0

S(1)=1 3 0. 1 0 0

1 0 20

Determine whether the new model is arbitrage free or not. If it is, find a state price vector. Determine whether the new model is complete or not. If so, find the risk neutral probability measure.

Please answer ASAP with full solutions and explanations!!

5. (1). Determine if the following model is arbitrage free: S(0)=(1,2,10),S(1)=11111230000010 If "Yes", find a state price vector; if the answer is "No", find an arbitrage trading strategy . (2) If S(0) remains the same but the payoff is changed to S(1)=11111230000020 Determine whether the new model is arbitrage free or not. If it is, find a state price vector. Determine whether the new model is complete or not. If so, find the risk neutral probability measure. 5. (1). Determine if the following model is arbitrage free: S(0)=(1,2,10),S(1)=11111230000010 If "Yes", find a state price vector; if the answer is "No", find an arbitrage trading strategy . (2) If S(0) remains the same but the payoff is changed to S(1)=11111230000020 Determine whether the new model is arbitrage free or not. If it is, find a state price vector. Determine whether the new model is complete or not. If so, find the risk neutral probability measureStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Short Term Financial Management

Authors: Terry S. Maness, John T. Zietlow

2nd Edition

0030315131, 978-0030315138