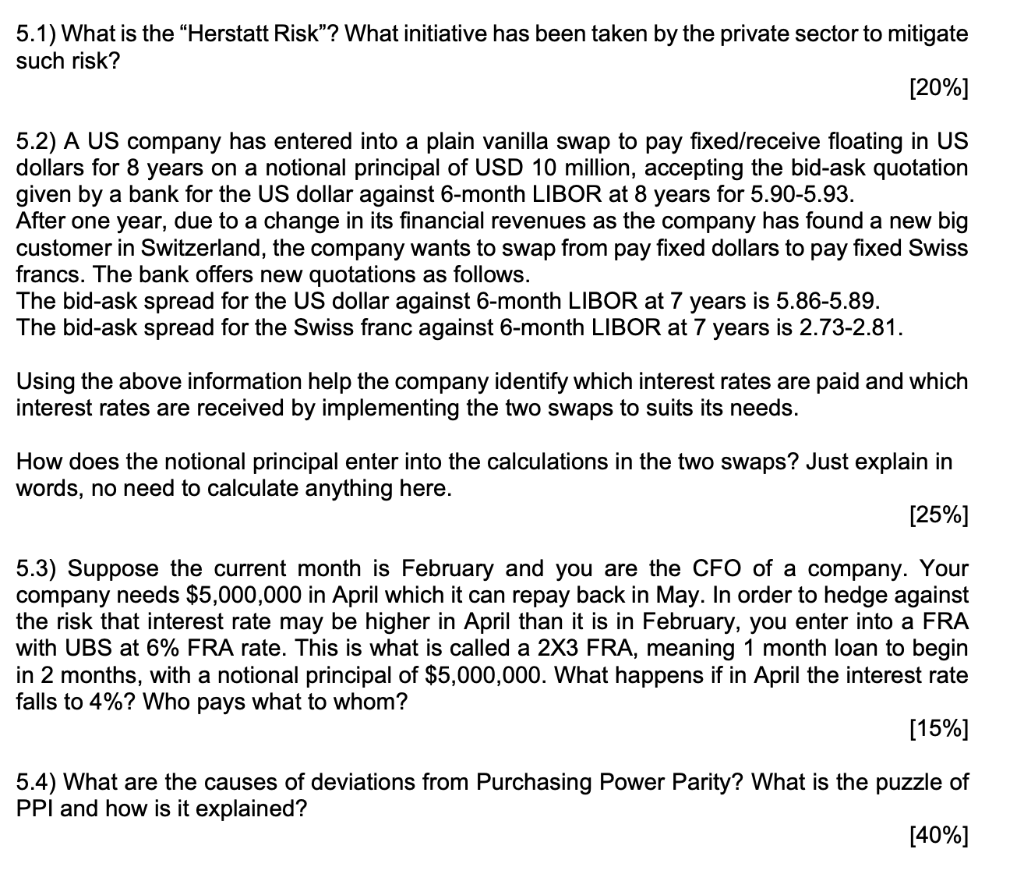

5.1) What is the Herstatt Risk"? What initiative has been taken by the private sector to mitigate such risk? [20%] 5.2) A US company has entered into a plain vanilla swap to pay fixed/receive floating in US dollars for 8 years on a notional principal of USD 10 million, accepting the bid-ask quotation given by a bank for the US dollar against 6-month LIBOR at 8 years for 5.90-5.93. After one year, due to a change in its financial revenues as the company has found a new big customer in Switzerland, the company wants to swap from pay fixed dollars to pay fixed Swiss francs. The bank offers new quotations as follows. The bid-ask spread for the US dollar against 6-month LIBOR at 7 years is 5.86-5.89. The bid-ask spread for the Swiss franc against 6-month LIBOR at 7 years is 2.73-2.81. Using the above information help the company identify which interest rates are paid and which interest rates are received by implementing the two swaps to suits its needs. How does the notional principal enter into the calculations in the two swaps? Just explain in words, no need to calculate anything here. [25%] 5.3) Suppose the current month is February and you are the CFO of a company. Your company needs $5,000,000 in April which it can repay back in May. In order to hedge against the risk that interest rate may be higher in April than it is in February, you enter into a FRA with UBS at 6% FRA rate. This is what is called a 2X3 FRA, meaning 1 month loan to begin in 2 months, with a notional principal of $5,000,000. What happens if in April the interest rate falls to 4%? Who pays what to whom? [15%] 5.4) What are the causes of deviations from Purchasing Power Parity? What is the puzzle of PPI and how is it explained? [40%] 5.1) What is the Herstatt Risk"? What initiative has been taken by the private sector to mitigate such risk? [20%] 5.2) A US company has entered into a plain vanilla swap to pay fixed/receive floating in US dollars for 8 years on a notional principal of USD 10 million, accepting the bid-ask quotation given by a bank for the US dollar against 6-month LIBOR at 8 years for 5.90-5.93. After one year, due to a change in its financial revenues as the company has found a new big customer in Switzerland, the company wants to swap from pay fixed dollars to pay fixed Swiss francs. The bank offers new quotations as follows. The bid-ask spread for the US dollar against 6-month LIBOR at 7 years is 5.86-5.89. The bid-ask spread for the Swiss franc against 6-month LIBOR at 7 years is 2.73-2.81. Using the above information help the company identify which interest rates are paid and which interest rates are received by implementing the two swaps to suits its needs. How does the notional principal enter into the calculations in the two swaps? Just explain in words, no need to calculate anything here. [25%] 5.3) Suppose the current month is February and you are the CFO of a company. Your company needs $5,000,000 in April which it can repay back in May. In order to hedge against the risk that interest rate may be higher in April than it is in February, you enter into a FRA with UBS at 6% FRA rate. This is what is called a 2X3 FRA, meaning 1 month loan to begin in 2 months, with a notional principal of $5,000,000. What happens if in April the interest rate falls to 4%? Who pays what to whom? [15%] 5.4) What are the causes of deviations from Purchasing Power Parity? What is the puzzle of PPI and how is it explained? [40%]