Answered step by step

Verified Expert Solution

Question

1 Approved Answer

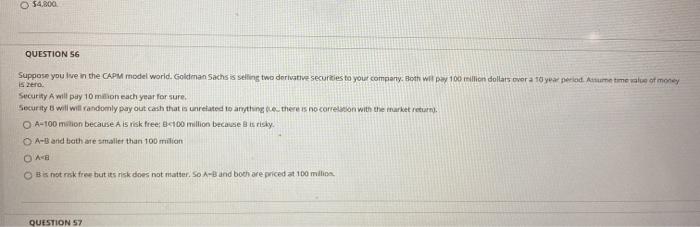

54.800 QUESTION SG Suppose you live in the CAPM model world. Goldman Sachsis selling two derivative securities to your company. Both we pay 100 million

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Planning Demystified A Self Teaching Guide

Authors: Paul Lim

1st Edition

0071476717,0071709711