Answered step by step

Verified Expert Solution

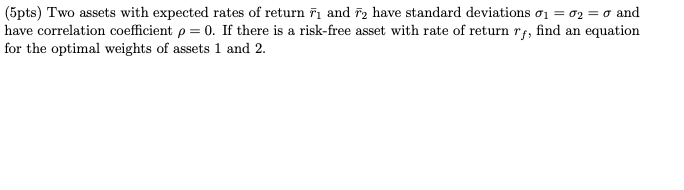

Question

1 Approved Answer

(5pts) Two assets with expected rates of return i and 2 have standard deviations ai = 02 a and have correlation coefficient p = 0.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Blockchain Real World Applications And Understanding How Blockchain Can Be Applied In Your World

Authors: Wayne Walker

1st Edition

1091858586, 978-1091858589