Answered step by step

Verified Expert Solution

Question

1 Approved Answer

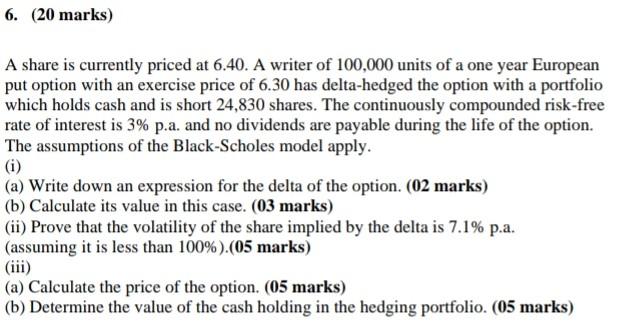

6. (20 marks) A share is currently priced at 6.40. A writer of 100,000 units of a one year European put option with an exercise

6. (20 marks) A share is currently priced at 6.40. A writer of 100,000 units of a one year European put option with an exercise price of 6.30 has delta-hedged the option with a portfolio which holds cash and is short 24,830 shares. The continuously compounded risk-free rate of interest is 3% p.a. and no dividends are payable during the life of the option. The assumptions of the Black-Scholes model apply. (i) (a) Write down an expression for the delta of the option. (02 marks) (b) Calculate its value in this case. (03 marks) (ii) Prove that the volatility of the share implied by the delta is 7.1% p.a. (assuming it is less than 100%).(05 marks) (iii) (a) Calculate the price of the option. (05 marks) (b) Determine the value of the cash holding in the hedging portfolio. (05 marks) 6. (20 marks) A share is currently priced at 6.40. A writer of 100,000 units of a one year European put option with an exercise price of 6.30 has delta-hedged the option with a portfolio which holds cash and is short 24,830 shares. The continuously compounded risk-free rate of interest is 3% p.a. and no dividends are payable during the life of the option. The assumptions of the Black-Scholes model apply. (i) (a) Write down an expression for the delta of the option. (02 marks) (b) Calculate its value in this case. (03 marks) (ii) Prove that the volatility of the share implied by the delta is 7.1% p.a. (assuming it is less than 100%).(05 marks) (iii) (a) Calculate the price of the option. (05 marks) (b) Determine the value of the cash holding in the hedging portfolio. (05 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Advanced Finance Theories

Authors: Ser-Huang Poon

1st Edition

9814460370, 978-9814460378