Answered step by step

Verified Expert Solution

Question

1 Approved Answer

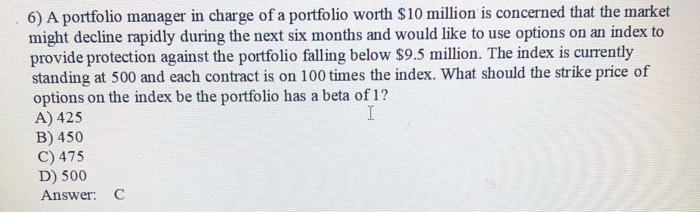

6) A portfolio manager in charge of a portfolio worth $10 million is concerned that the market might decline rapidly during the next six months

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Guide To Rental Property Investing And Management

Authors: Alex Turner

1st Edition

979-8856074641