Question

6. A U.S. Corporate treasurer will receive a 2 million payment in 30 days from a British customer. The treasurer has no strong opinion about

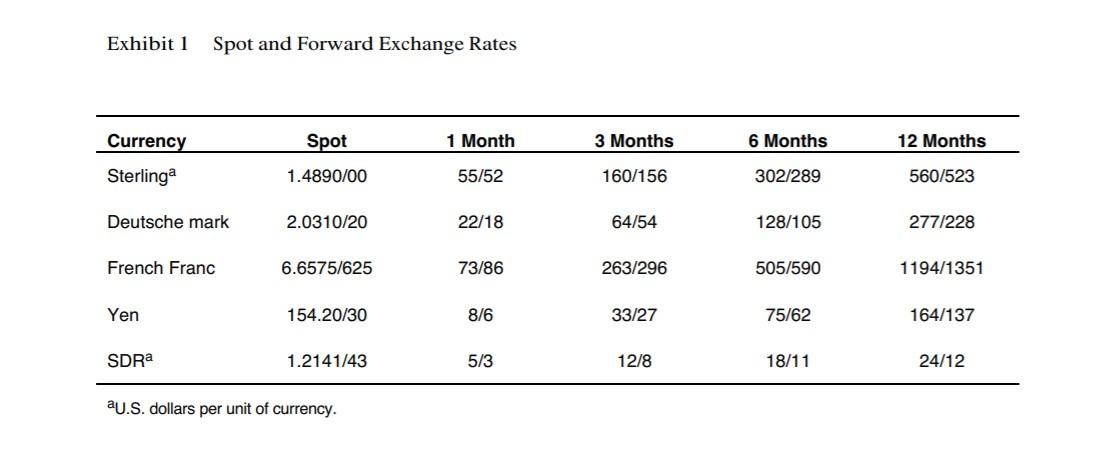

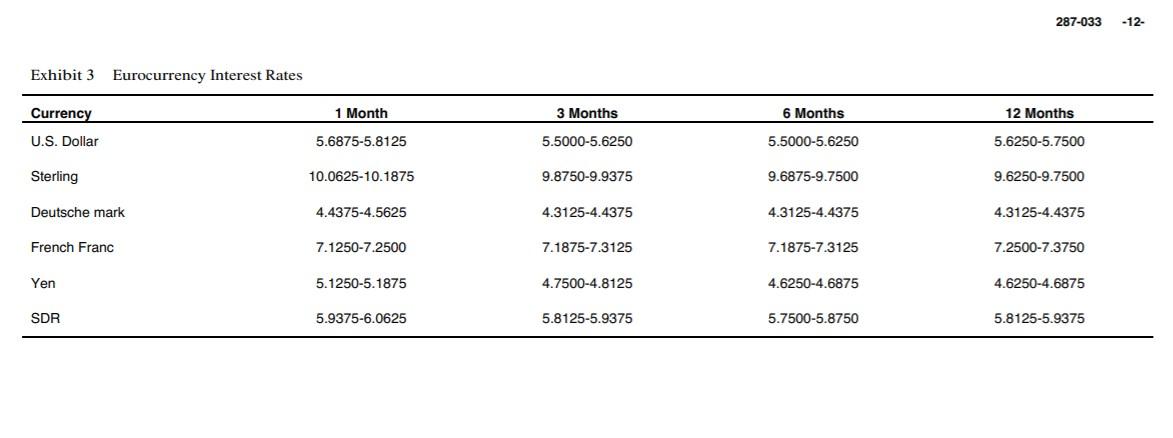

6. A U.S. Corporate treasurer will receive a 2 million payment in 30 days from a British customer. The treasurer has no strong opinion about the direction or magnitude of changes in the sterling spot rate but would like to eliminate the uncertainty surrounding such movements. Within the context of the rates shown in Exhibits 1 and 3, what options are available to the treasurer for hedging the foreign exchange risk associated with the sterling payment? What is the expected cost (expressed as an annualized percentage) of each alternative? Which alternative should the treasurer pursue? How would your answers to the above questions change if the treasurer believed very strongly that sterling would trade at $1.45?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Decentralized Finance How DeFi Is Changing The Future Of Money

Authors: Rhian Lewis

1st Edition

1398609390, 978-1398609396