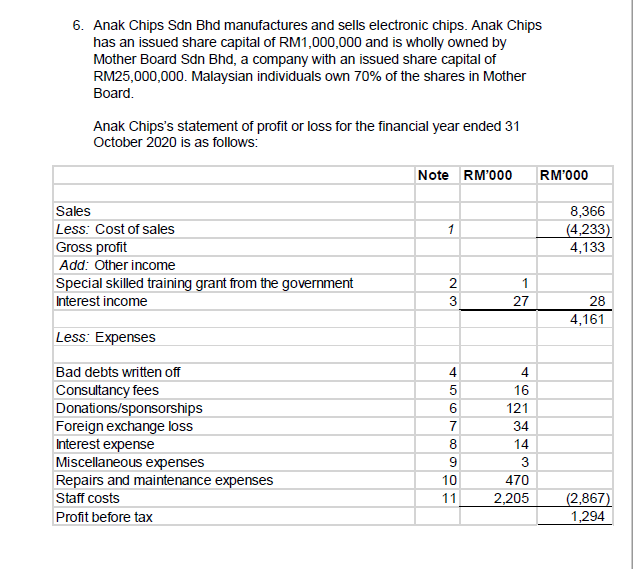

6. Anak Chips Sdn Bhd manufactures and sells electronic chips. Anak Chips has an issued share capital of RM1,000,000 and is wholly owned by Mother Board Sdn Bhd, a company with an issued share capital of RM25,000,000. Malaysian individuals own 70% of the shares in Mother Board. Anak Chipss statement of profit or loss for the financial year ended 31 October 2020 is as follows:

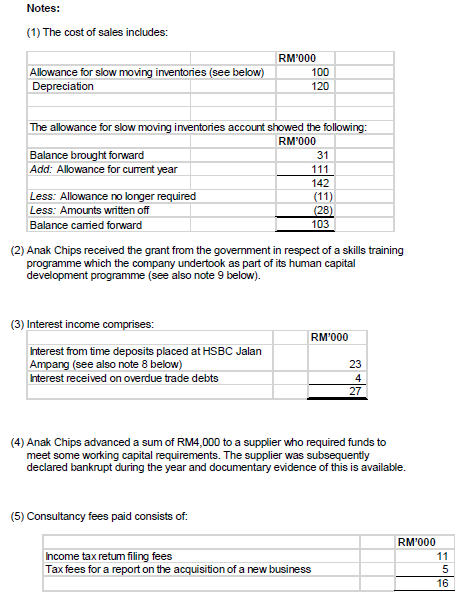

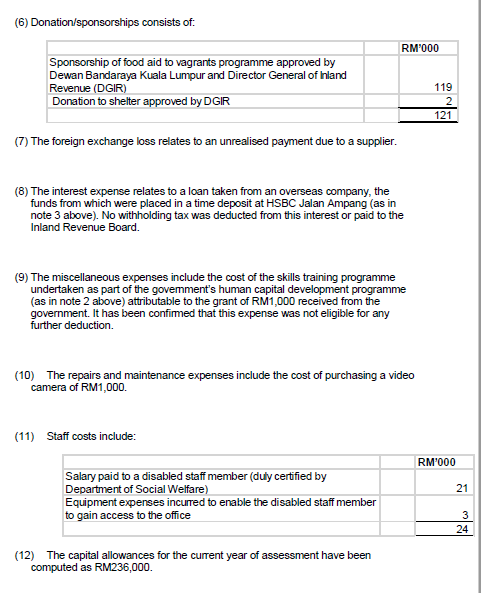

6. Anak Chips Sdn Bhd manufactures and sells electronic chips. Anak Chips has an issued share capital of RM1,000,000 and is wholly owned by Mother Board Sdn Bhd, a company with an issued share capital of RM25,000,000. Malaysian individuals own 70% of the shares in Mother Board. Anak Chips's statement of profit or loss for the financial year ended 31 October 2020 is as follows: Notes: (1) The cost of sales includes: (2) Anak Chips received the grant from the government in respect of a skills training programme which the company undertook as part of its human capital development programme (see also note 9 below). (3 (4) Anak Chips advanced a sum of RM4,000 to a supplier who required funds to meet some working capital requirements. The supplier was subsequently declared bankrupt during the year and documentary evidence of this is available. (5) Consultancy fees paid consists of: (6) Donation/sponsorships consists of: (7) The foreign exchange loss relates to an unrealised payment due to a supplier. (8) The interest expense relates to a loan taken from an overseas company, the funds from which were placed in a time deposit at HSBC Jalan Ampang (as in note 3 above). No withholding tax was deducted from this interest or paid to the Inland Revenue Board. (9) The miscellaneous expenses include the cost of the skills training programme undertaken as part of the govemment's human capital development programme (as in note 2 above) attributable to the grant of RM1,000 received from the government. It has been confirmed that this expense was not eligible for any further deduction. (10) The repairs and maintenance expenses include the cost of purchasing a video camera of RM1,000. (11) Staff costs include: (12) The capital allowances for the current year of assessment have been computed as RM236,000. Required: (a) Compute the chargeable income and income tax payable by Anak Chips Sdn Bhd for the year of assessment 2020. Note: You should indicate by the use of the word 'nil' any item referred to in the question for which no adjusting entry needs to be made in the tax computation. [30 marks] (b) Explain rational behind the introduction of "withholding tax" in Malaysia. [10 marks] (c) Provide the compliance requirements how a Anak Chips Sdn Bhd can claim capital allowance under schedule 3 of the Income Tax Act 1967 (as amended). [10 marks] 6. Anak Chips Sdn Bhd manufactures and sells electronic chips. Anak Chips has an issued share capital of RM1,000,000 and is wholly owned by Mother Board Sdn Bhd, a company with an issued share capital of RM25,000,000. Malaysian individuals own 70% of the shares in Mother Board. Anak Chips's statement of profit or loss for the financial year ended 31 October 2020 is as follows: Notes: (1) The cost of sales includes: (2) Anak Chips received the grant from the government in respect of a skills training programme which the company undertook as part of its human capital development programme (see also note 9 below). (3 (4) Anak Chips advanced a sum of RM4,000 to a supplier who required funds to meet some working capital requirements. The supplier was subsequently declared bankrupt during the year and documentary evidence of this is available. (5) Consultancy fees paid consists of: (6) Donation/sponsorships consists of: (7) The foreign exchange loss relates to an unrealised payment due to a supplier. (8) The interest expense relates to a loan taken from an overseas company, the funds from which were placed in a time deposit at HSBC Jalan Ampang (as in note 3 above). No withholding tax was deducted from this interest or paid to the Inland Revenue Board. (9) The miscellaneous expenses include the cost of the skills training programme undertaken as part of the govemment's human capital development programme (as in note 2 above) attributable to the grant of RM1,000 received from the government. It has been confirmed that this expense was not eligible for any further deduction. (10) The repairs and maintenance expenses include the cost of purchasing a video camera of RM1,000. (11) Staff costs include: (12) The capital allowances for the current year of assessment have been computed as RM236,000. Required: (a) Compute the chargeable income and income tax payable by Anak Chips Sdn Bhd for the year of assessment 2020. Note: You should indicate by the use of the word 'nil' any item referred to in the question for which no adjusting entry needs to be made in the tax computation. [30 marks] (b) Explain rational behind the introduction of "withholding tax" in Malaysia. [10 marks] (c) Provide the compliance requirements how a Anak Chips Sdn Bhd can claim capital allowance under schedule 3 of the Income Tax Act 1967 (as amended). [10 marks]