Answered step by step

Verified Expert Solution

Question

1 Approved Answer

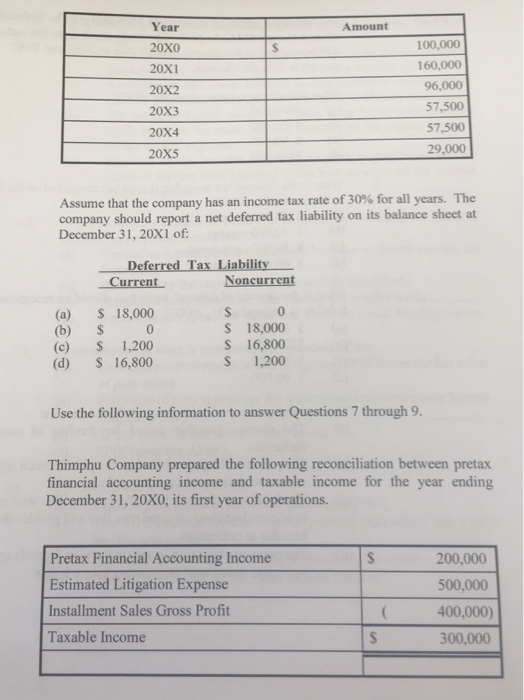

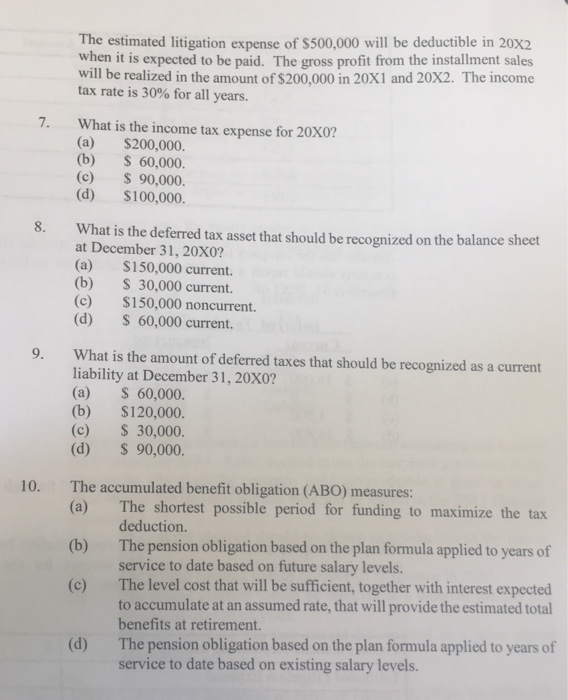

6. Dhaka Corporation purchased an asset on January 2, 20X0, for $500,000. The computer has an estimated useful life of five years with no salvage

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Unofficial Guide To Medical Research Audit And Teaching

Authors: Ceen-Ming Tang BA BM BCh MRCGP, Colin Fischbacher, Zeshan Qureshi BM BSc MSc MRCPCH FAcadMEd MRCPS

1st Edition

0957149980, 978-0957149984