Answered step by step

Verified Expert Solution

Question

1 Approved Answer

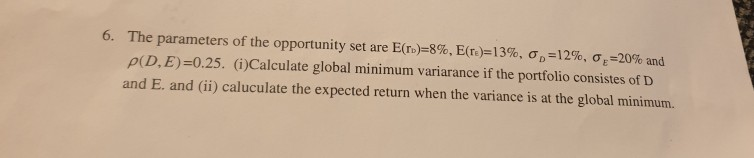

6. The parameters of the opportunity set are E(T))=8%, E(re)=13%, 0,=12%, 0 -20% and P(D,E)=0.25. (i)Calculate global minimum variarance if the portfolio consistes of D

6. The parameters of the opportunity set are E(T))=8%, E(re)=13%, 0,=12%, 0 -20% and P(D,E)=0.25. (i)Calculate global minimum variarance if the portfolio consistes of D and E. and (ii) caluculate the expected return when the variance is at the global minimum

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance At The Threshold

Authors: Christopher Houghton Budd

1st Edition

0566092115, 978-0566092114