Answered step by step

Verified Expert Solution

Question

1 Approved Answer

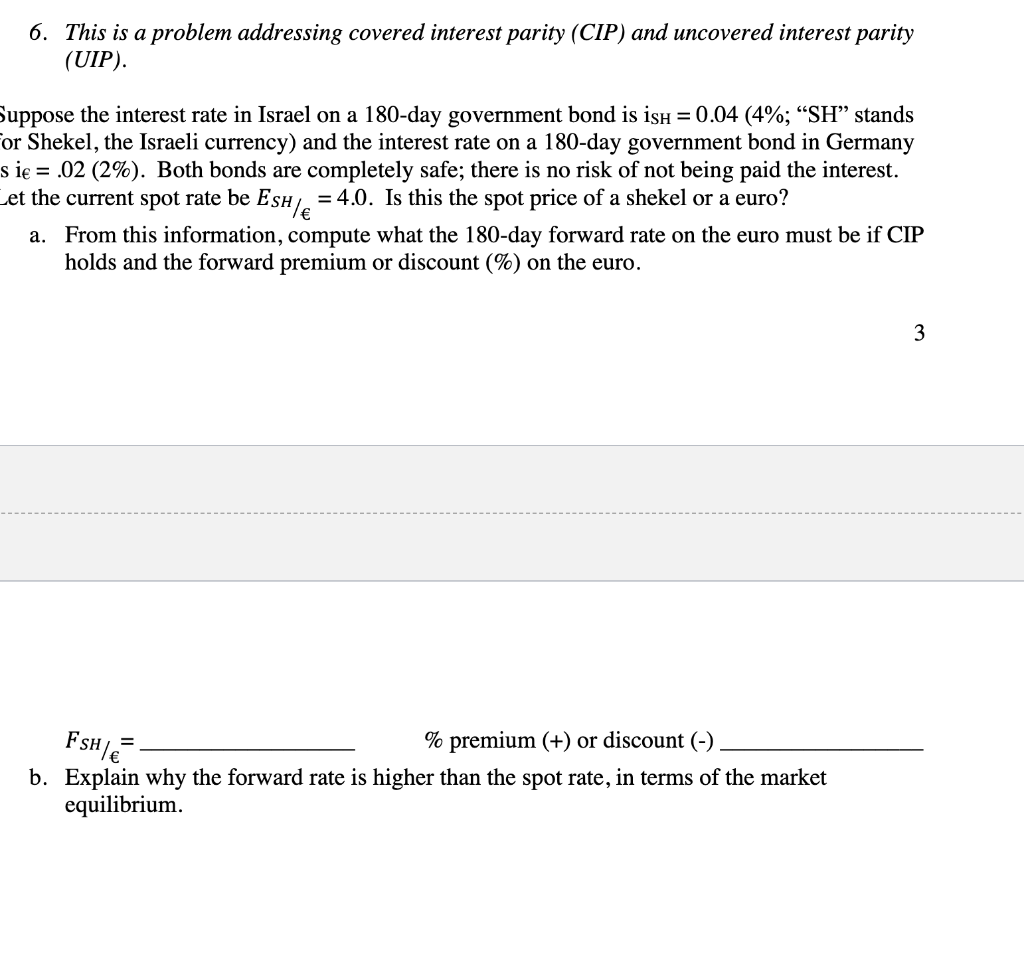

6. This is a problem addressing covered interest parity (CIP) and uncovered interest parity (UIP). Suppose the interest rate in Israel on a 180-day government

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Terrorist Finance

Authors: T. Wittig

2011th Edition

0230291848, 978-0230291843