Answered step by step

Verified Expert Solution

Question

1 Approved Answer

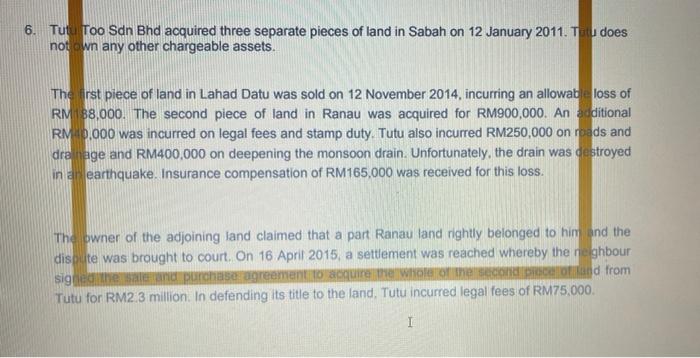

6. Tutu Too Sdn Bhd acquired three separate pieces of land in Sabah on 12 January 2011. Te does not own any other chargeable assets.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Tail Risk Hedging Creating Robust Portfolios For Volatile Markets

Authors: Vineer Bhansali

1st Edition

0071791752,0071791760