Answered step by step

Verified Expert Solution

Question

1 Approved Answer

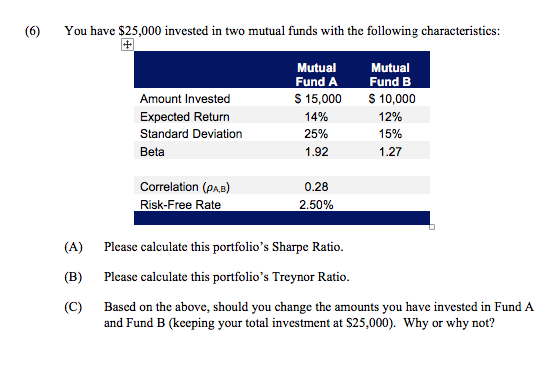

(6) You have $25,000 invested in two mutual funds with the following characteristics: Amount Invested Expected Return Standard Deviation Beta Mutual Fund A $ 15,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microfinance And Sustainable Development In Africa

Authors: Yahaya Alhassan, Uzoechi Nwagbara

1st Edition

1799874990,1799875024