Answered step by step

Verified Expert Solution

Question

1 Approved Answer

6.Compute CAPM beta of the hedge fund as of 12/31/2020. The answer should be given in decimal form (e.g., 1 % is 0.01). Hint: the

6.Compute CAPM beta of the hedge fund as of 12/31/2020. The answer should be given in decimal form (e.g., 1 % is 0.01). Hint: the sign matters!

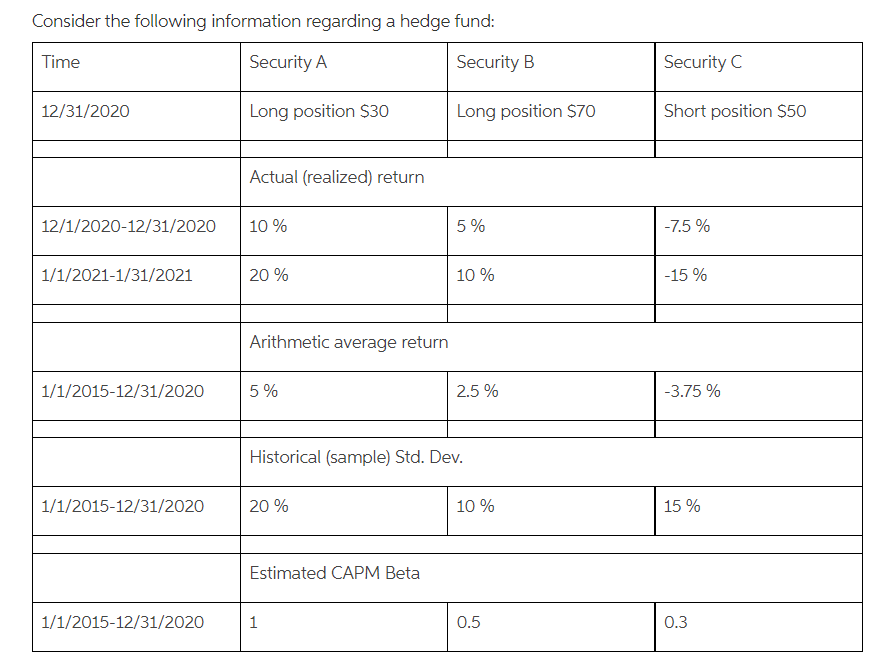

Consider the following information regarding a hedge fund: Time Security A Security B Security C 12/31/2020 Long position $30 Long position $70 Short position $50 Actual realized) return 12/1/2020-12/31/2020 10 % 5 % -7.5 % 1/1/2021-1/31/2021 20 % 10 % -15% Arithmetic average return 1/1/2015-12/31/2020 5 % 2.5 % -3.75 % Historical (sample) Std. Dev. 1/1/2015-12/31/2020 20 % 10 % 15 % Estimated CAPM Beta 1/1/2015-12/31/2020 1 0.5 0.3Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essays In Finance

Authors: Robert Giffen

1st Edition

111629088X, 9781116290882