Answered step by step

Verified Expert Solution

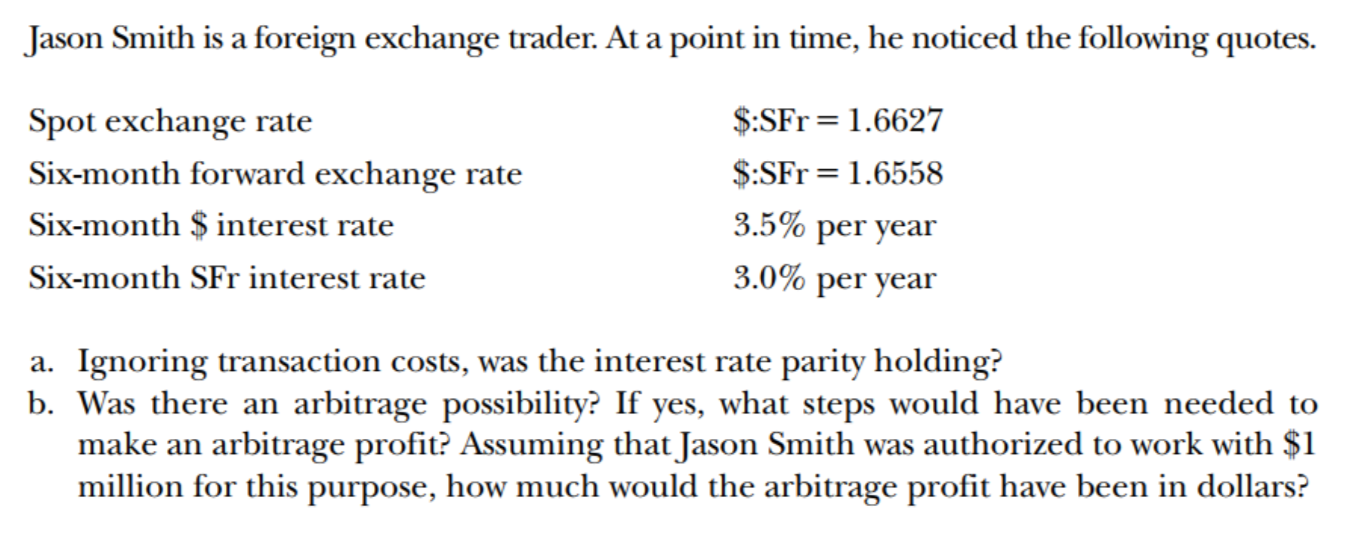

Question

1 Approved Answer

7 Answer a Please explain where are For six months, r SFr => 1.50% and r $ => 1.75%. came from? I don't understand this

7

Answer a

Please explain where are "For six months, rSFr => 1.50% and r$ => 1.75%." came from? I don't understand this part.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Marketing

Authors: Philip R Cateora

14th Edition

0073380989, 9780073380988