Answered step by step

Verified Expert Solution

Question

1 Approved Answer

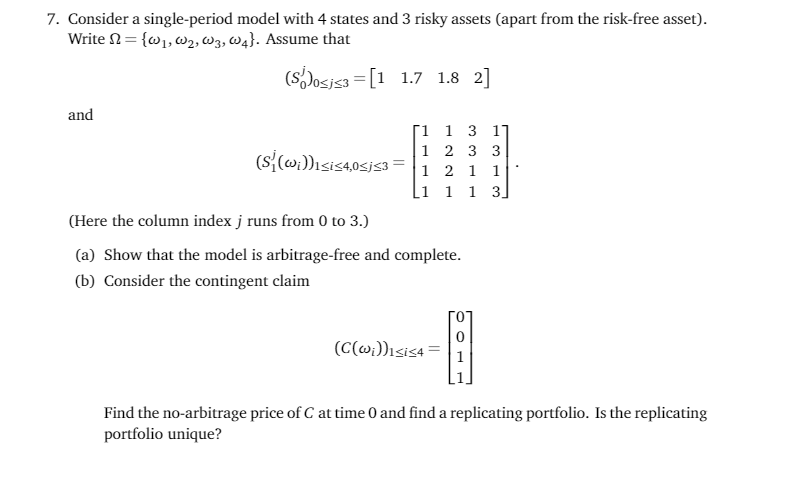

7. Consider a single-period model with 4 states and 3 risky assets (apart from the risk-free asset). Write 1={w1, 62, 63, 64}. Assume that (5))osis3

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Investing In Todays Financial Markets

Authors: Alessandro De Cristofaro

1st Edition

1070350931, 978-1070350936