Answered step by step

Verified Expert Solution

Question

1 Approved Answer

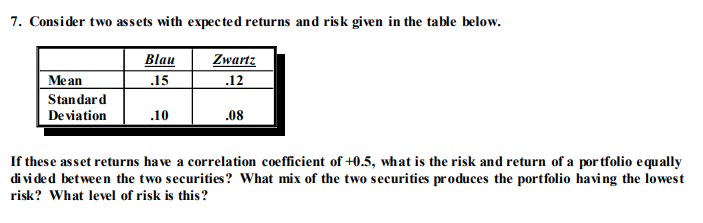

7. Consider two assets with expected returns and risk given in the table below. Blau 115 Zwartz Me an Stan dard De viation .12 .10

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Renewable Energy Finance Theory And Practice

Authors: Santosh Raikar, Seabron Adamson

1st Edition

0128164417, 9780128164419