Answered step by step

Verified Expert Solution

Question

1 Approved Answer

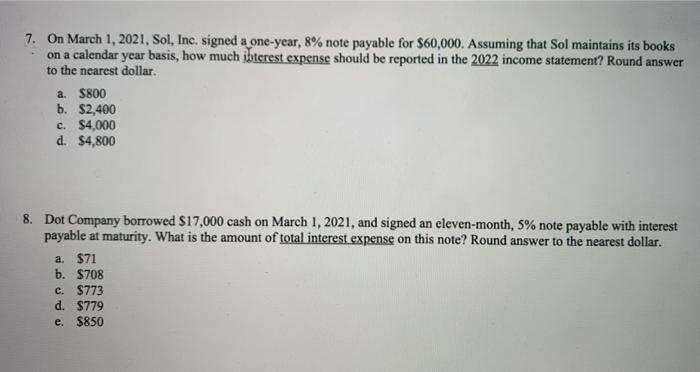

7. On March 1, 2021, Sol, Inc. signed a one-year, 8% note payable for $60,000. Assuming that Sol maintains its books on a calendar year

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

IRS Audit Protection And Survival Guide Trucking Industry

Authors: Daniel J. Baran, Gerald F. Bernard, James E. Brown

1st Edition

0471166413, 978-0471166412