Answered step by step

Verified Expert Solution

Question

1 Approved Answer

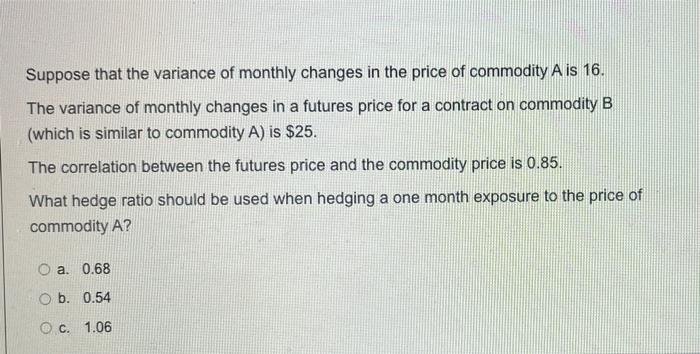

7. Suppose that the variance of monthly changes in the price of commodity A is 16. The variance of monthly changes in a futures price

7.

Suppose that the variance of monthly changes in the price of commodity A is 16. The variance of monthly changes in a futures price for a contract on commodity B (which is similar to commodity A) is $25. The correlation between the futures price and the commodity price is 0.85. What hedge ratio should be used when hedging a one month exposure to the price of commodity A? O a. 0.68 O b. 0.54 OC. 1.06 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Retail Investor In Focus The Indian IPO Experience

Authors: Parimala Veluvali

1st Edition

3030127559,3030127567