Answered step by step

Verified Expert Solution

Question

1 Approved Answer

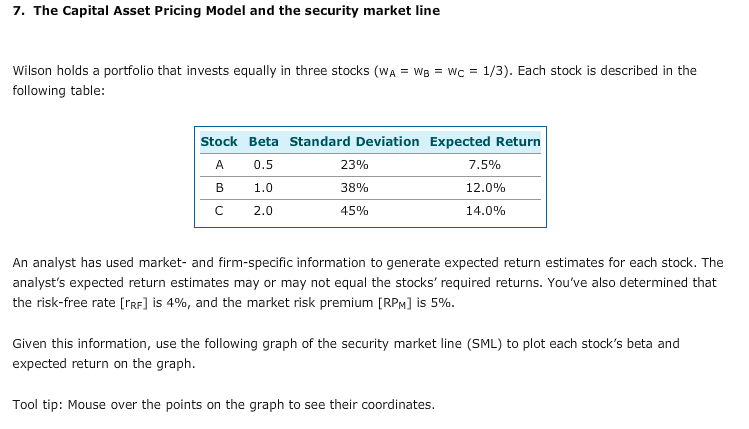

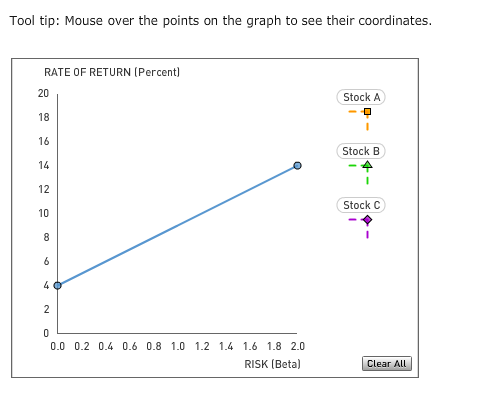

7. The Capital Asset Pricing Model and the security market line Wilson holds a portfolio that invests equally in three stocks (WA = We =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Professionally Managed Assets A Definitive Guide To Profiting From Alternative Investments

Authors: Keith Fevurly

1st Edition

143026019X, 978-1430260196