Answered step by step

Verified Expert Solution

Question

1 Approved Answer

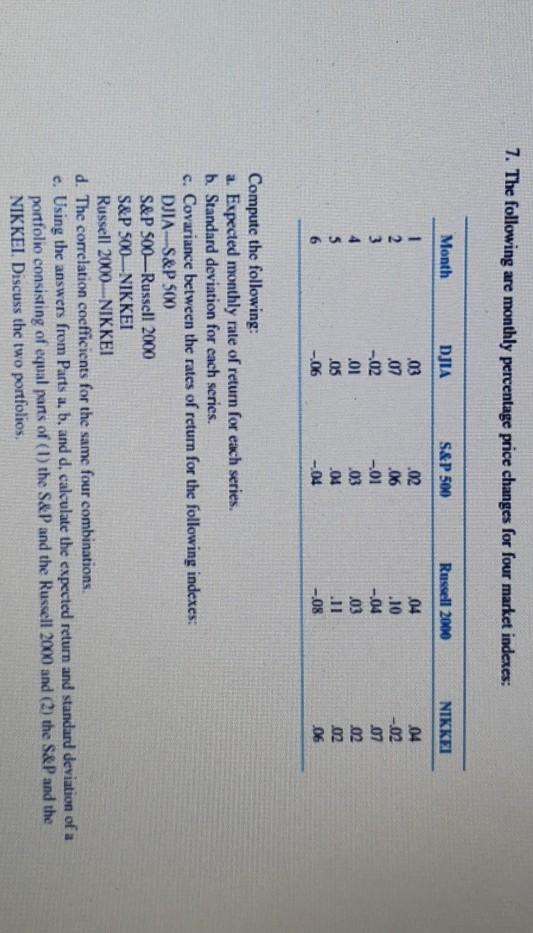

7. The following are monthly percentage price changes for four market indexes: Month DJIA S&P 500 Russell 2000 NIKKEL 1 2 3 4 5 6

7. The following are monthly percentage price changes for four market indexes: Month DJIA S&P 500 Russell 2000 NIKKEL 1 2 3 4 5 6 03 .07 -02 .01 .05 --06 .02 .06 --01 .03 .04 -04 .04 .10 -.04 .03 .11 -08 04 -.02 .07 .02 .02 06 Compute the following: a. Expected monthly rate of return for each series. b. Standard deviation for each series. c. Covariance between the rates of return for the following indexes: DJIA S&P 500 S&P 500Russell 2000 S&P 500 NIKKEI Russell 2000 NIKKEI d. The correlation coefficients for the same four combinations c. Using the answers from Parts a, b, and d, calculate the expected return and standard deviation of a portfolio consisting of equal parts of (1) the S&P and the Russell 2000 and (2) the S&P and the NIKKEI. Discuss the two portfolios

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Passive Income Ideas 2020 $10 000 Per Month Ultimate Guide

Authors: Roberts Ronald

1st Edition

1951595793, 978-1951595791