Answered step by step

Verified Expert Solution

Question

1 Approved Answer

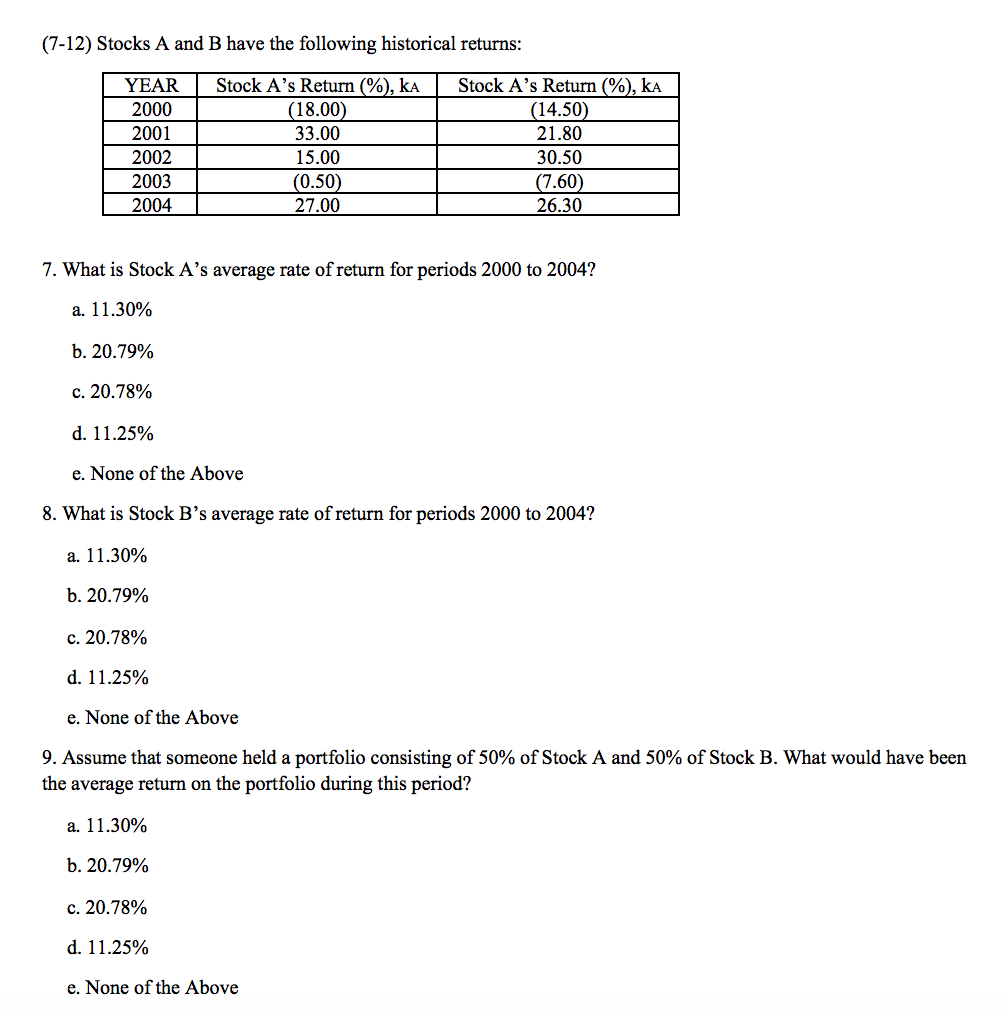

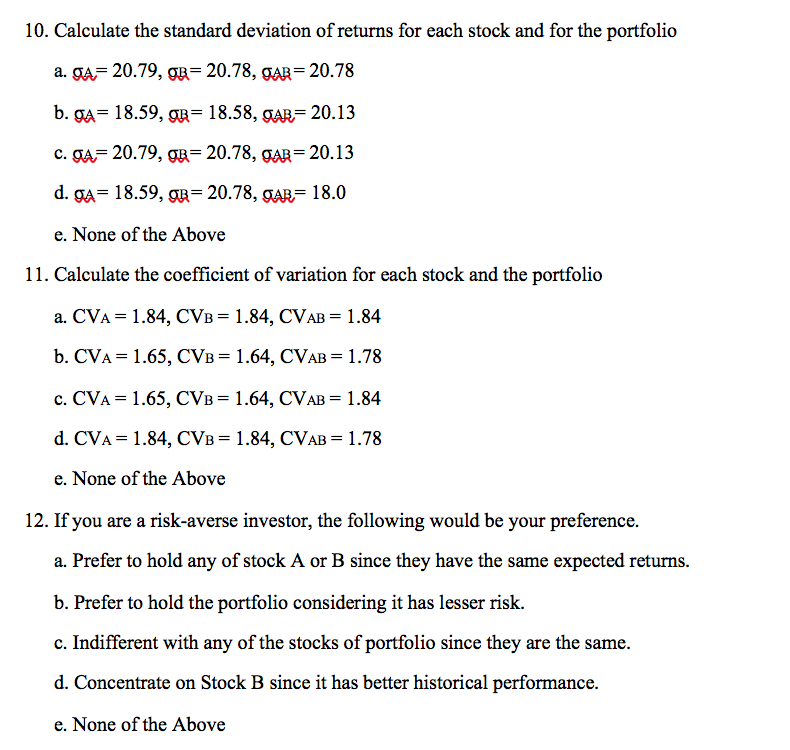

(7-12) Stocks A and B have the following historical returns: YEAR 2000 2001 2002 2003 2004 Stock A's Return (%), KA (18.00) 33.00 15.00 (0.50)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of Income Distribution Volume 2A

Authors: Anthony B. Atkinson, Francois Bourguignon

1st Edition

0444594280, 978-0444594280