Answered step by step

Verified Expert Solution

Question

1 Approved Answer

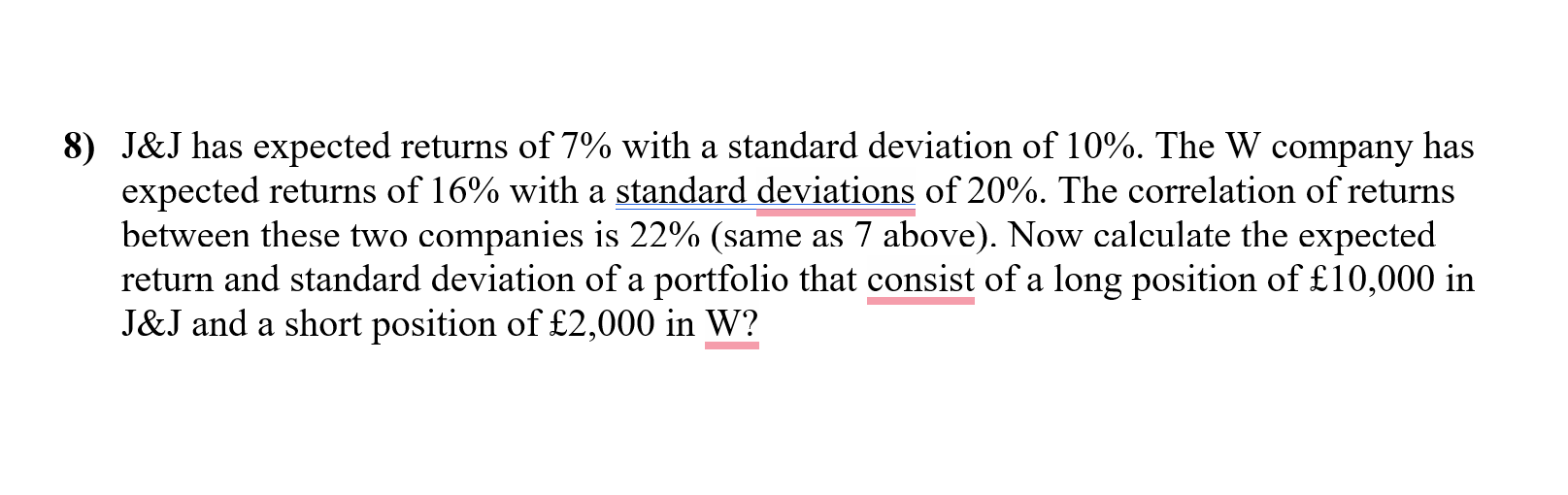

8) J&J has expected returns of 7% with a standard deviation of 10%. The W company has expected returns of 16% with a standard deviations

8) J&J has expected returns of 7% with a standard deviation of 10%. The W company has expected returns of 16% with a standard deviations of 20%. The correlation of returns between these two companies is 22% (same as 7 above). Now calculate the expected return and standard deviation of a portfolio that consist of a long position of 10,000 in J&J and a short position of 2,000 in W

8) J&J has expected returns of 7% with a standard deviation of 10%. The W company has expected returns of 16% with a standard deviations of 20%. The correlation of returns between these two companies is 22% (same as 7 above). Now calculate the expected return and standard deviation of a portfolio that consist of a long position of 10,000 in J&J and a short position of 2,000 in W Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Times Guide To Finance For Non Financial Managers

Authors: Jo Haigh

1st Edition

0273756206, 978-0273756200