Question

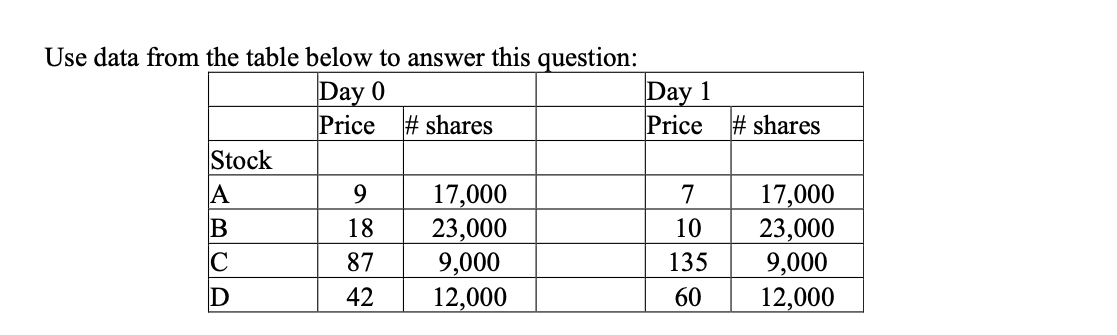

(8 points) The value-weighted index on day 0 is computed with only the three stocks A, B and C. The index value on day 0

-

(8 points) The value-weighted index on day 0 is computed with only the three stocks A, B and C. The index value on day 0 is 100.

-

Compute the divisor on day 0.

-

What is the return on the value-weighted index on day 1?

-

Stock C is split 5-for-1 after the close of Day 1. What is the divisor for the value-weighted index after the split?

-

After the close of market on Day 1, Stock C is replaced by Stock D in the value-weighted index, and the new index is computed with only Stocks A, B and D. Compute the new divisor and the index value after this change to the index composition.

-

-

(2 points) The equal-weighted index on day 0 is computed with only the three stocks A, B and C. What is the return on the equal-weighted index on day 1?

d. (6 points) You plan to track each of these three indices (with only the three stocks A, B and C). Suppose you have $1,000,000 to invest on day 0, and you are allowed to buy fractional shares.

-

How many shares of each stock would you buy on day 0 to track (a) the price- weighted index (b) the value-weighted index and (c) the equal-weighted index?

-

How many shares of each stock would you buy on day 1 to track (a) the price- weighted index (b) the value-weighted index and (c) the equal-weighted index?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Climate Finance

Authors: Richard B. Stewart, Benedict Kingsbury, Bryce Rudyk

1st Edition

081474138X, 978-0814741382