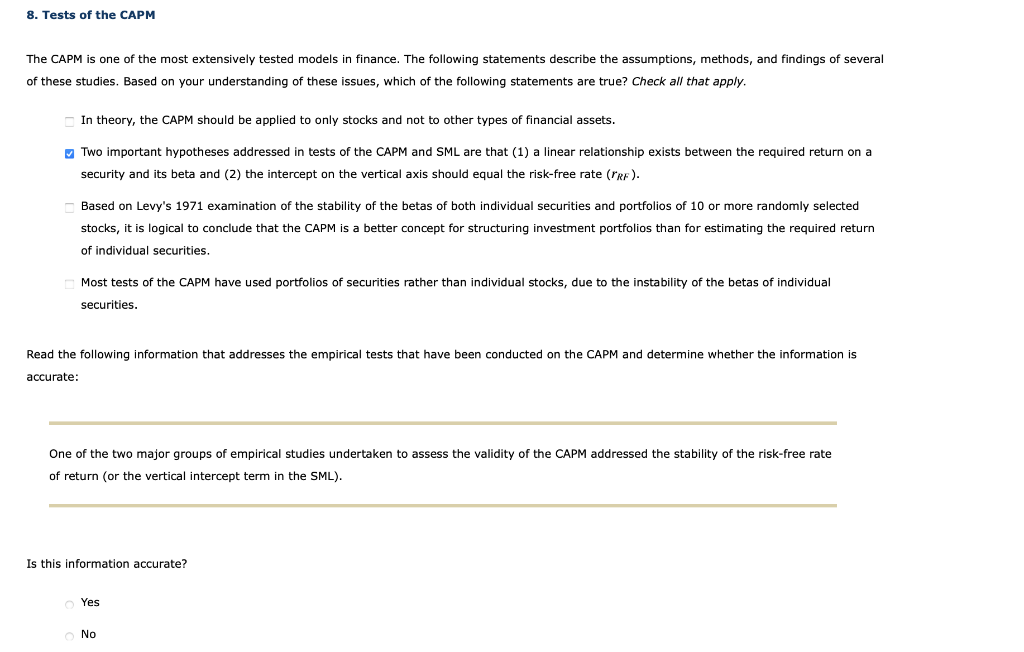

8. Tests of the CAPM The CAPM is one of the most extensively tested models in finance. The following statements describe the assumptions, methods, and findings of several of these studies. Based on your understanding of these issues, which of the following statements are true? Check all that apply In theory, the CAPM should be applied to only stocks and not to other types of financial assets. Two important hypotheses addressed in tests of the CAPM and SML are that (1) a linear relationship exists between the required return on a security and its beta and (2) the intercept on the vertical axis should equal the risk-free rate (TRF). Based on Levy's 1971 examination of the stability of the betas of both individual securities and portfolios of 10 or more randomly selected stocks, it is logical to conclude that the CAPM is a better concept for structuring investment portfolios than for estimating the required return of individual securities. Most tests of the CAPM have used portfolios of securities rather than individual stocks, due to the instability of the betas of individual securities. Read the following information that addresses the empirical tests that have been conducted on the CAPM and determine whether the information is accurate: One of the two major groups of empirical studies undertaken to assess the validity of the CAPM addressed the stability of the risk-free rate of return (or the vertical intercept term in the SML). Is this information accurate? Yes No 8. Tests of the CAPM The CAPM is one of the most extensively tested models in finance. The following statements describe the assumptions, methods, and findings of several of these studies. Based on your understanding of these issues, which of the following statements are true? Check all that apply In theory, the CAPM should be applied to only stocks and not to other types of financial assets. Two important hypotheses addressed in tests of the CAPM and SML are that (1) a linear relationship exists between the required return on a security and its beta and (2) the intercept on the vertical axis should equal the risk-free rate (TRF). Based on Levy's 1971 examination of the stability of the betas of both individual securities and portfolios of 10 or more randomly selected stocks, it is logical to conclude that the CAPM is a better concept for structuring investment portfolios than for estimating the required return of individual securities. Most tests of the CAPM have used portfolios of securities rather than individual stocks, due to the instability of the betas of individual securities. Read the following information that addresses the empirical tests that have been conducted on the CAPM and determine whether the information is accurate: One of the two major groups of empirical studies undertaken to assess the validity of the CAPM addressed the stability of the risk-free rate of return (or the vertical intercept term in the SML). Is this information accurate? Yes No