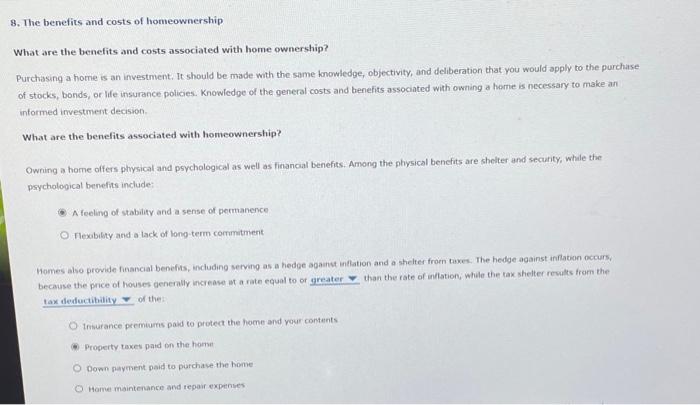

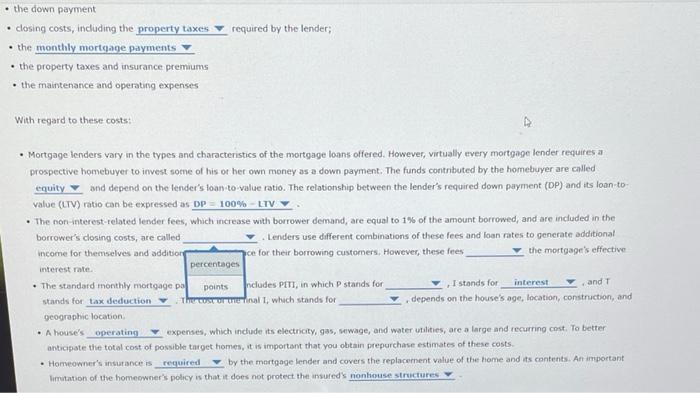

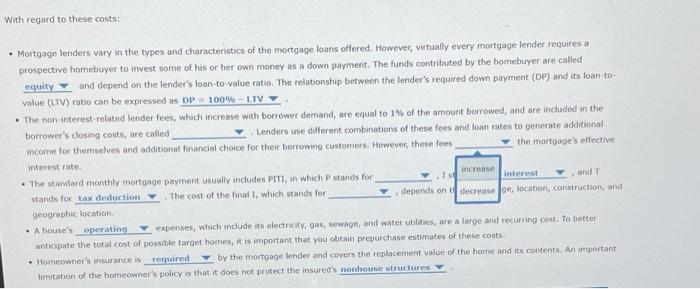

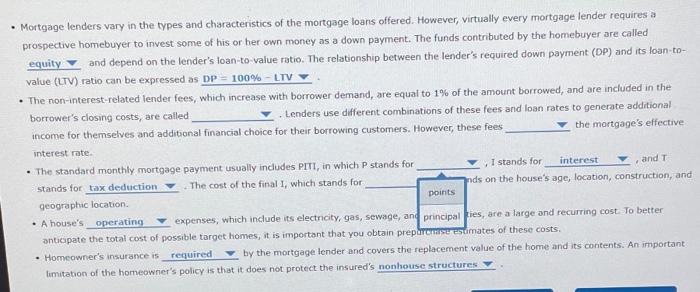

8. The benefits and costs of homeownership What are the benefits and costs associated with home ownership? Purchasing a home is an investment. It should be made with the same knowledge, objectivity, and deliberation that you would apply to the purchase of stocks, bonds, or life insurance policies. Knowledge of the general costs and benefits associated with owning a home is necessary to make an informed investment decision What are the benefits associated with homeownership? Owning a home offers physical and psychological as well as financial benefits. Among the physical benefits are shelter and security, while the psychological benefits include: A feeling of stability and a sense of permanence Flexibility and a lack of long term commitment Homes also provide financial benefits, including serving as a hedge against inflation and a shelter from time. The hedge against Inflation occurs because the price of houses generally increase tarate equal to or greater than the rate of inflation, while the tax shelter results from the tax deductibility of the Onwurance premium paid to protect the home and your contents Property taxes paid on the home Down payment paid to purchase the home Home maintenance and repair expenses required by the lender; the down payment closing costs, including the property taxes the monthly mortgage payments the property taxes and insurance premiums . the maintenance and operating expenses . With regard to these costs: Mortgage lenders vary in the types and characteristics of the mortgage loans offered. However, virtually every mortgage lender requires a prospective homebuyer to invest some of his or her own money as a down payment. The funds contributed by the homebuyer are called equity and depend on the bender's loan to value ratio. The relationship between the lender's required down payment (DP) and its loan to value (LTV) ratio can be expressed as DP = 100% - LTV The non-interest-related lender fees, which increase with borrower demand, are equal to 1% of the amount borrowed, and are included in the borrower's closing costs, are called Lenders use different combinations of these fees and loan rates to generate additional income for themselves and addition ce for their borrowing customers. However, these fees the mortgage's effective interest rate percentages The standard monthly mortgage pa points Includes PITI, in which stands for I stands for interest stands for tax deduction The cost finall, which stands for depends on the house's age, location, construction, and geographic location . A house's operating expenses, which include its electricity, gas, sewage, and water utilities, are a large and recurring cost. To better anticipate the total cost of possible to get homes, it is important that you obtain prepurchase estimates of these costs Homeowner's insurance is required by the mortgage lender and covers the replacement value of the home and its contents. An important limitation of the homeowner's policy is that it does not protect the insured's nonhouse structures and T With regard to these costs: Mortgage lenders vary in the types and characteristics of the mortgage loans offered. However, virtually every mortgage lender requires a prospective homebuyer to invest some of his or her own money as a down payment. The funds contributed by the homebuyer are called equity and depend on the lender's loan-to-value ratio. The relationship between the lender's required down payment (DP) and its loan to- value (LTV) ratio can be expressed as DP 100% LIV The non interest-related lender fees, which increase with borrower demand, are equal to 1% of the amount borrowed, and are included in the borrower's closing costs, are called Lenders use different combinations of these fees and loan rates to generate additional income for themselves and additional financial choice for their borrowing customers. However, these fees the mortgages effective interest rate increase The standard monthly mortgage payment usually includes PITI, in which stands for internet stands for tax deduction The cost of the finall, which stands for depends on decrease Joe, location, construction, and geographic location - A house's operating expenses, which include its electricity, gas, sewage, and water utilities, are a large and recurring cost. To better anticipate the total cost of possible target homes, it is important that you obtain prepurchase estimates of these costs Homeowner's insurance is required by the mortgage lender and covers the replacement value of the home and its contents. An important limitation of the homeowner's policy is that it does not protect the insured's nonhouse structures and Mortgage lenders vary in the types and characteristics of the mortgage loans offered. However, virtually every mortgage lender requires a prospective homebuyer to invest some of his or her own money as a down payment. The funds contributed by the homebuyer are called equity and depend on the lender's loan to value ratio. The relationship between the lender's required down payment (DP) and its loan-to- value (LTV) ratio can be expressed as DP = 100% - LTV The non-interest-related lender fees, which increase with borrower demand, are equal to 1% of the amount borrowed, and are included in the borrower's closing costs, are called Lenders use different combinations of these fees and loan rates to generate additional income for themselves and additional financial choice for their borrowing customers. However, these fees the mortgage's effective interest rate The standard monthly mortgage payment usually includes PITI, in which P stands for I stands for interest and T stands for tax deduction The cost of the final I, which stands for inds on the house's age, location, construction, and geographic location points A house's operating expenses, which include its electricity, gas, sewage, and principalies, are a large and recurring cost. To better anticipate the total cost of possible target homes, it is important that you obtain preprise estimates of these costs. Homeowner's insurance is required by the mortgage lender and covers the replacement value of the home and its contents. An important limitation of the homeowner's policy is that it does not protect the insured's nonhouse structures characteristics of the mortgage loans offered. However, virtually every mortgage lender rec of his or her own money as a down payment. The funds contributed by the homebuyer are er's loan-to-value ratio. The relationship between the lender's required down payment (DP) am DP = 100% - LTV which increase with borrower demand, are equal to 1% of the amount borrowed, and are inclu . Lenders use different combinations of these fees and loan rates to generate financial choice for their borrowing customers. However, these fees the mortga ment usually includes PITI, in which P stands for e cost of the final I, which stands for , I stands for interest depends on the house's age, location, co insurance mses, which include its electricity, gas, water utilities, are a large and recurring cost. target homes, it is important that you index rate chase estimates of these costs. ed by the mortgage lender and covers the replacement value of the home and its contents. y is that it does not protect the insured's nonhouse structures