Answered step by step

Verified Expert Solution

Question

1 Approved Answer

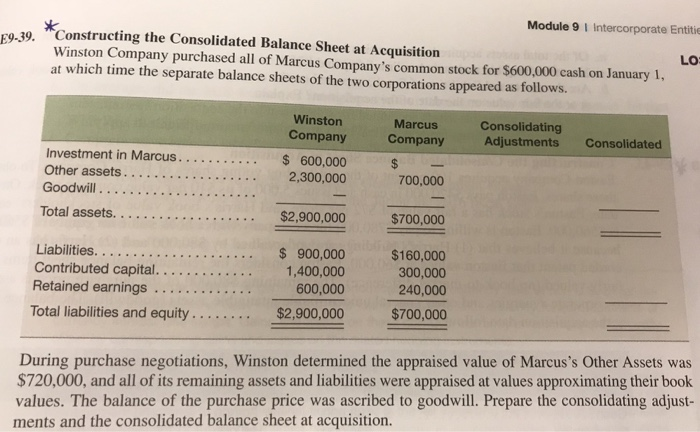

9 I Intercorporate Entities e Interpreting Equity Method Investment Footnotes AT& T reports the following footnote to its 2015 10-K report. X E9-37. Equity Method

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing and Accounting Cases Investigating Issues of Fraud and Professional Ethics

Authors: Jay Thibodeau, Deborah Freier

4th edition

78025567, 978-0078025563