Answered step by step

Verified Expert Solution

Question

1 Approved Answer

9. please help fill in the 4 incorrect boxes Listed below are selected transactions of Wildhorse Department Store for the current year ending December 31.

9.

please help fill in the 4 incorrect boxes

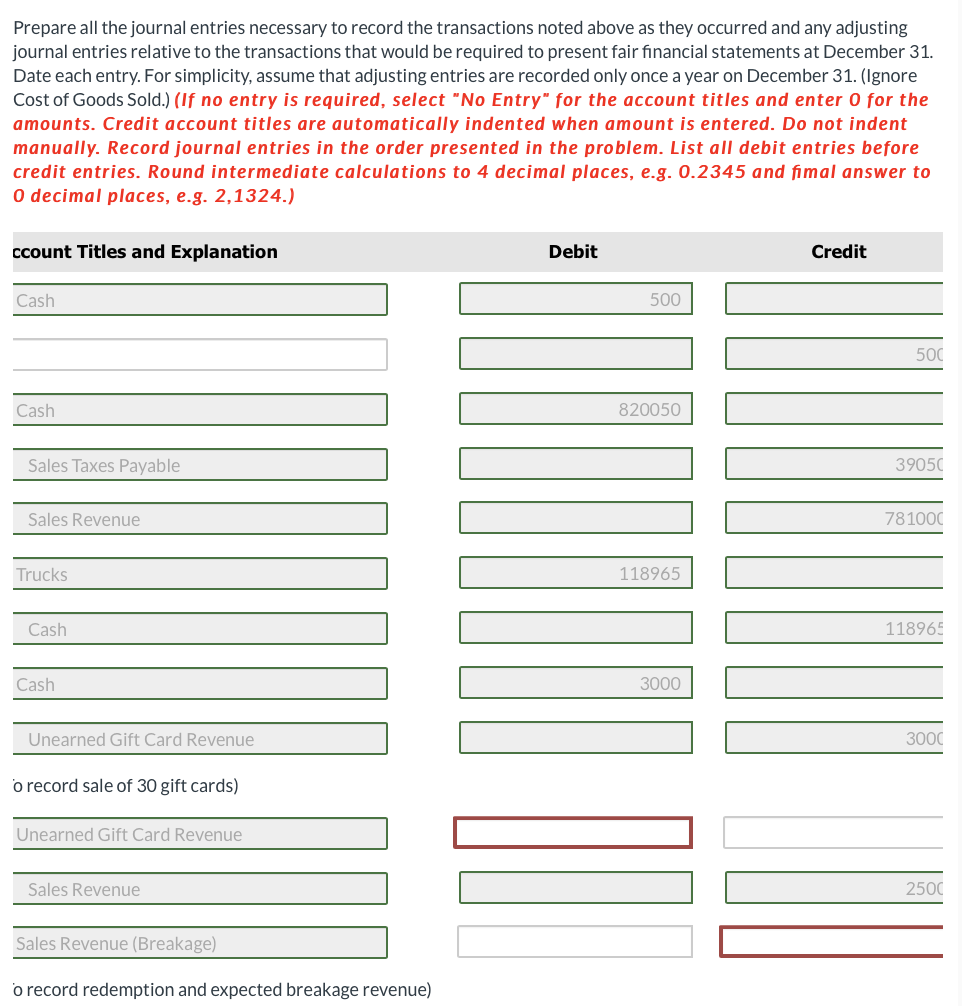

Listed below are selected transactions of Wildhorse Department Store for the current year ending December 31. 1. On December 5 , the store received $500 from the Selig Players as a deposit to be returned after certain furniture to be used in stage production was returned on January 15. 2. During December, cash sales totaled $820,050, which includes the 5% sales tax that must be remitted to the state by the fifteenth day of the following month. 3. On December 10 , the store purchased for cash three delivery trucks for $113,300. The trucks were purchased in a state that applies a 5% sales tax. 4. The store sold 30 gift cards for $100 per card. At year-end, 25 of the gift cards are redeemed. Wildhorse expects three of the cards to expire unused. Prepare all the journal entries necessary to record the transactions noted above as they occurred and any adjusting journal entries relative to the transactions that would be required to present fair financial statements at December 31 . Date each entry. For simplicity, assume that adjusting entries are recorded only once a year on December 31. (Ignore Cost of Goods Sold.) (If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Credit account titles are automatically indented when amount is entered. Do not indent manually. Record journal entries in the order presented in the problem. List all debit entries before credit entries. Round intermediate calculations to 4 decimal places, e.g. 0.2345 and fimal answer to 0 decimal places, e.g. 2,1324.) Prepare all the journal entries necessary to record the transactions noted above as they occurred and any adjusting journal entries relative to the transactions that would be required to present fair financial statements at December 31 . Date each entry. For simplicity, assume that adjusting entries are recorded only once a year on December 31. (Ignore Cost of Goods Sold.) (If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Credit account titles are automatically indented when amount is entered. Do not indent manually. Record journal entries in the order presented in the problem. List all debit entries before credit entries. Round intermediate calculations to 4 decimal places, e.g. 0.2345 and fimal answer to 0 decimal places, e.g. 2,1324.)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Loss Control Auditing A Guide For Conducting Fire Safety And Security Audits

Authors: E. Scott Dunlap

2nd Edition

103244293X, 978-1032442938