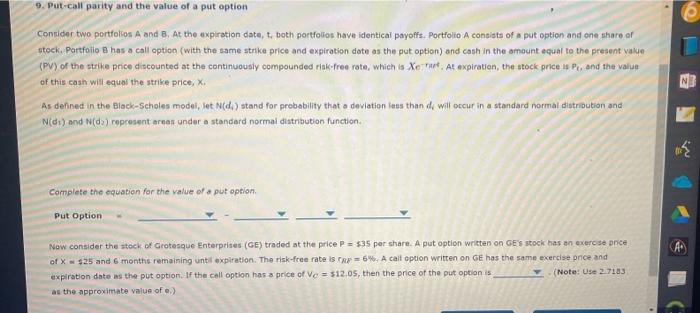

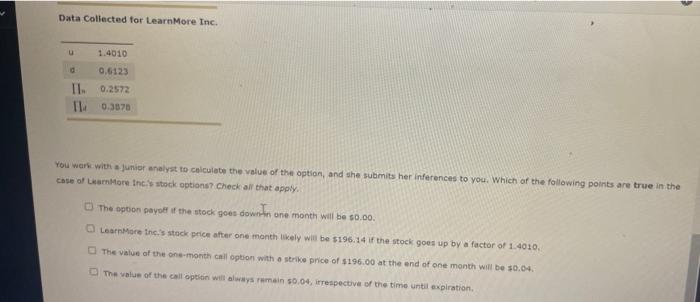

9. Put-call parity and the value of a put option Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free rate, which is Xe rart. At expiration, the stock price is P, and the value of this cash will equal the strike price, X. As defined in the Black-Scholes model, let N(d) stand for probability that a deviation less than de will occur in a standard normal distribution and N(ds) and N(d) represent areas under a standard normal distribution function. Complete the equation for the value of a put option. Put Option Now consider the stock of Grotesque Enterprises (GE) traded at the price P= $35 per share. A put option written on GE's stock has an exercise price of X $25 and 6 months remaining until expiration. The risk-free rate is rar 6%. A call option written on GE has the same exercise price and expiration date as the put option. If the cell option has a price of Ve $12.05, then the price of the put option is (Note: Use 2.7183 as the approximate value of e.) Data Collected for LearnMore Inc. u 1.4010 0.6123 II 0.2572 11 0.3878 You work with a junior analyst to calculate the value of the option, and she submits her inferences to you. Which of the following points are true in the case of LearnMore Inc.'s stock options? Check all that apply. The option payoff if the stock goes downin one month will be $0.00. LearnMore Inc.'s stock price after one month likely will be $196.14 if the stock goes up by a factor of 1.4010. The value of the one-month call option with a strike price of $196.00 at the end of one month will be $0.04. The value of the call option will always remain $0.04, irrespective of the time until expiration. id 9. Put-call parity and the value of a put option Consider two portfolios A and B. At the expiration date, t, both portfolios have identical payoffs. Portfolio A consists of a put option and one share of stock. Portfolio B has a call option (with the same strike price and expiration date as the put option) and cash in the amount equal to the present value (PV) of the strike price discounted at the continuously compounded risk-free rate, which is Xe rart. At expiration, the stock price is P, and the value of this cash will equal the strike price, X. As defined in the Black-Scholes model, let N(d) stand for probability that a deviation less than de will occur in a standard normal distribution and N(ds) and N(d) represent areas under a standard normal distribution function. Complete the equation for the value of a put option. Put Option Now consider the stock of Grotesque Enterprises (GE) traded at the price P= $35 per share. A put option written on GE's stock has an exercise price of X $25 and 6 months remaining until expiration. The risk-free rate is rar 6%. A call option written on GE has the same exercise price and expiration date as the put option. If the cell option has a price of Ve $12.05, then the price of the put option is (Note: Use 2.7183 as the approximate value of e.) Data Collected for LearnMore Inc. u 1.4010 0.6123 II 0.2572 11 0.3878 You work with a junior analyst to calculate the value of the option, and she submits her inferences to you. Which of the following points are true in the case of LearnMore Inc.'s stock options? Check all that apply. The option payoff if the stock goes downin one month will be $0.00. LearnMore Inc.'s stock price after one month likely will be $196.14 if the stock goes up by a factor of 1.4010. The value of the one-month call option with a strike price of $196.00 at the end of one month will be $0.04. The value of the call option will always remain $0.04, irrespective of the time until expiration. id