Answered step by step

Verified Expert Solution

Question

1 Approved Answer

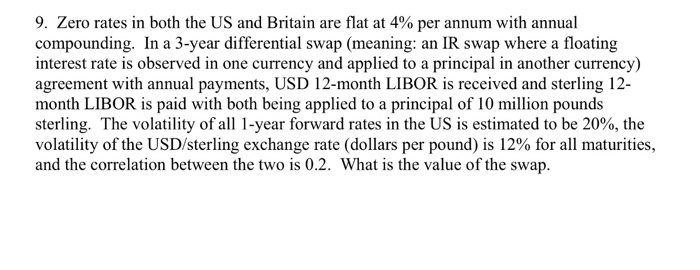

9, Zero rates in both the US and Britain are flat at 4% per annum with annual compounding. In a 3-year differential swap (meaning: an

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Entrepreneurial Finance

Authors: J . chris leach, Ronald w. melicher

4th edition

538478152, 978-0538478151