Answered step by step

Verified Expert Solution

Question

1 Approved Answer

9&10 please and thank you QUESTION 9 Which of the following statements is true? A. Bond prices vary directly with interest rates. B. High coupon

9&10 please and thank you

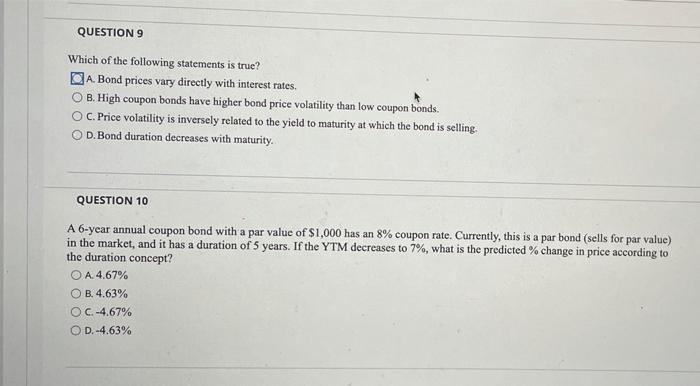

QUESTION 9 Which of the following statements is true? A. Bond prices vary directly with interest rates. B. High coupon bonds have higher bond price volatility than low coupon bonds. OC. Price volatility is inversely related to the yield to maturity at which the bond is selling O D. Bond duration decreases with maturity. QUESTION 10 A 6-year annual coupon bond with a par value of $1,000 has an 8% coupon rate. Currently, this is a par bond (sells for par value) in the market, and it has a duration of 5 years. If the YTM decreases to 7%, what is the predicted % change in price according to the duration concept? O A.4.67% OB. 4.63% O C.-4.67% OD.-4.63% Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Introduces Quantitative Finance

Authors: Paul Wilmott

2nd edition

470319585, 470319581, 978-0470319581