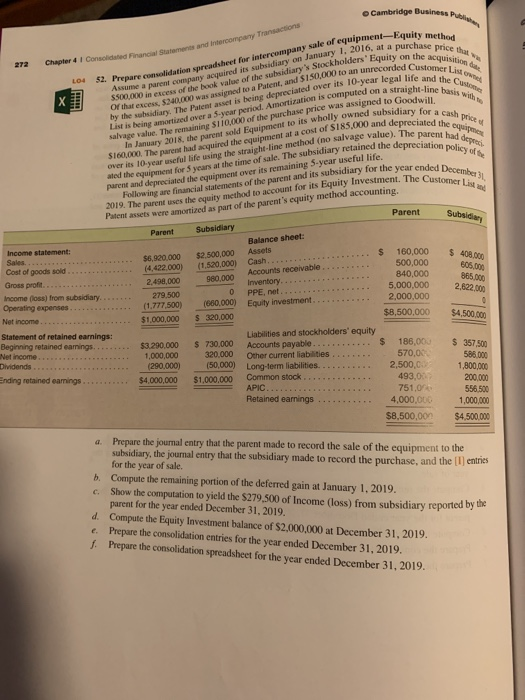

Cambridge Business Pus Chapter 41 Consolidated Financial Statements and intercompany Transactions 52. Prepare consolidation spreadsheet for intercompany sale of equipment-Equity method Assume a parent company acquired its subsidiary on January 1. 2016, at a purchase price that S500,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition by the subsidiary. The Parent asset is being depreciated over its 10-year legal life and the Customer List is being amortized over a 5-year period. Amortization is computed on a straight-line basis what Or that excess, 5240.000 was assigned to a Patent, and $150,000 to an unrecorded Customer Lido salvage value. The remaining ST10,000 of the purchase price was assigned to Goodwill. In January 2018, the parent sold Equipment to its wholly owned subsidiary for a cash price ated the equipment for years at the time of sale. The subsidiary retained the depreciation policy of the over its 10-year useful life using the straight-line method (no salvage value). The parent had depre. 2019. The puremates the equity method to account for its Equity Investment. The Customer List Following are financial statements of the parent and its subsidiary for the year ended December S100,000. The parent had acquired the equipment at a cost of $185.000 and depreciated the equat 272 LOG 0111 parent and depreciated the equipment over its remaining 5-year useful life. Parent Patent assets were amortized as part of the parent's equity method accounting. Subsidiary Parent Subsidiary $6,920,000 (4.422.000) 2.498,000 279.500 (1.777.500) $1,000,000 Balance sheet: Assets Cash Accounts receivable Inventory PPE, net Equity Investment $2,500,000 (1.520,000) 980,000 0 (660,000) $ 320,000 Income statement: Sales... Cost of goods sold Gross profit.. Income (loss) from subsidiary. Operating expenses Net Income Statement of retained earnings: Beginning retained earnings. Net income.. Dividends. Ending retained earnings $ 160,000 500,000 840,000 5,000,000 2,000,000 $8,500,000 $408.000 806.000 865.000 2,622.000 $4.500.000 $ $3.290.000 1,000,000 (290,000) $4,000,000 $ 730,000 320,000 (50,000) $1,000,000 Liabilities and stockholders' equity Accounts payable Other current liabilities Long-term liabilities. Common stock APIC. Retained earnings 186,000 570,00 2,500.00 493,00 751,00 4,000,000 $8,500,000 $ 357.500 586.000 1,800,000 200.000 556.500 1,000,000 $4,500,000 c. Prepare the journal entry that the parent made to record the sale of the equipment to the subsidiary, the journal entry that the subsidiary made to record the purchase, and the (1) entries for the year of sale. b. Compute the remaining portion of the deferred gain at January 1, 2019. Show the computation to yield the $279.500 of Income (loss) from subsidiary reported by the parent for the year ended December 31, 2019, d. Compute the Equity Investment balance of $2,000,000 at December 31, 2019. Prepare the consolidation entries for the year ended December 31, 2019. 1. Prepare the consolidation spreadsheet for the year ended December 31, 2019. Cambridge Business Pus Chapter 41 Consolidated Financial Statements and intercompany Transactions 52. Prepare consolidation spreadsheet for intercompany sale of equipment-Equity method Assume a parent company acquired its subsidiary on January 1. 2016, at a purchase price that S500,000 in excess of the book value of the subsidiary's Stockholders' Equity on the acquisition by the subsidiary. The Parent asset is being depreciated over its 10-year legal life and the Customer List is being amortized over a 5-year period. Amortization is computed on a straight-line basis what Or that excess, 5240.000 was assigned to a Patent, and $150,000 to an unrecorded Customer Lido salvage value. The remaining ST10,000 of the purchase price was assigned to Goodwill. In January 2018, the parent sold Equipment to its wholly owned subsidiary for a cash price ated the equipment for years at the time of sale. The subsidiary retained the depreciation policy of the over its 10-year useful life using the straight-line method (no salvage value). The parent had depre. 2019. The puremates the equity method to account for its Equity Investment. The Customer List Following are financial statements of the parent and its subsidiary for the year ended December S100,000. The parent had acquired the equipment at a cost of $185.000 and depreciated the equat 272 LOG 0111 parent and depreciated the equipment over its remaining 5-year useful life. Parent Patent assets were amortized as part of the parent's equity method accounting. Subsidiary Parent Subsidiary $6,920,000 (4.422.000) 2.498,000 279.500 (1.777.500) $1,000,000 Balance sheet: Assets Cash Accounts receivable Inventory PPE, net Equity Investment $2,500,000 (1.520,000) 980,000 0 (660,000) $ 320,000 Income statement: Sales... Cost of goods sold Gross profit.. Income (loss) from subsidiary. Operating expenses Net Income Statement of retained earnings: Beginning retained earnings. Net income.. Dividends. Ending retained earnings $ 160,000 500,000 840,000 5,000,000 2,000,000 $8,500,000 $408.000 806.000 865.000 2,622.000 $4.500.000 $ $3.290.000 1,000,000 (290,000) $4,000,000 $ 730,000 320,000 (50,000) $1,000,000 Liabilities and stockholders' equity Accounts payable Other current liabilities Long-term liabilities. Common stock APIC. Retained earnings 186,000 570,00 2,500.00 493,00 751,00 4,000,000 $8,500,000 $ 357.500 586.000 1,800,000 200.000 556.500 1,000,000 $4,500,000 c. Prepare the journal entry that the parent made to record the sale of the equipment to the subsidiary, the journal entry that the subsidiary made to record the purchase, and the (1) entries for the year of sale. b. Compute the remaining portion of the deferred gain at January 1, 2019. Show the computation to yield the $279.500 of Income (loss) from subsidiary reported by the parent for the year ended December 31, 2019, d. Compute the Equity Investment balance of $2,000,000 at December 31, 2019. Prepare the consolidation entries for the year ended December 31, 2019. 1. Prepare the consolidation spreadsheet for the year ended December 31, 2019