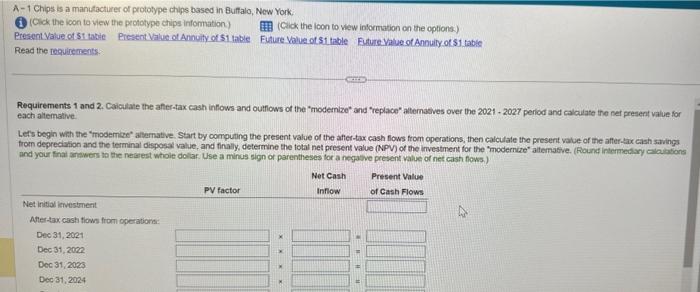

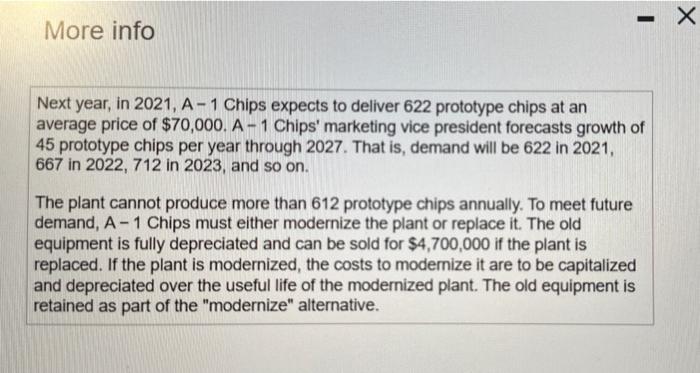

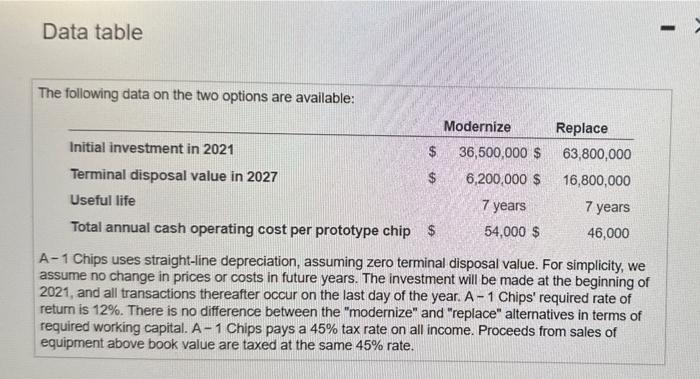

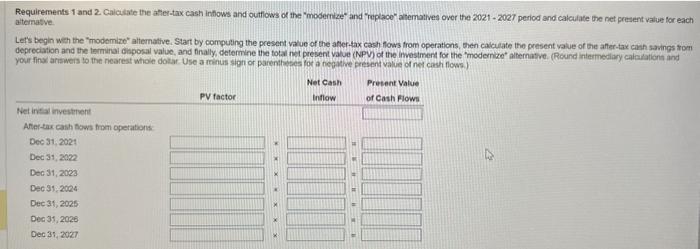

A - 1 Chips is a manutacturer of prototype chlps based in Bulfalo, Now York: (1) (Cick the icon to wew the prototype chips infomation.) Present Value. of Si tabie Present Value of Annuily of 51 lable IIA (Cick the ioon to view inlormation on the options) Read the roguicicients: Euture Value of Annuly of 51 table Requirements 1 and 2. Calculate the after-tax cash inflows and outflows of the "modemize" and "replace" altemasves over the 2021 - 2027 period and calculate the net present value for each altemative. Lefs begin whh the "modemiee" aharnative. Start by computing the present value of the affer-tax cash flows from operations, then calculate the present value of the affer tax eash savigs from depreclation and the terminal disposal value, and finally, determine the total net present value (NPV) of the investinent for the "modernize" attemative. (fiound internectary oriatitions and your finai answors to the neasest whoie dollar. Use a minus sign or parentheses for a negasve present value of net cish fows.) Next year, in 2021, A-1 Chips expects to deliver 622 prototype chips at an average price of $70,000. A 1 Chips' marketing vice president forecasts growth of 45 prototype chips per year through 2027. That is, demand will be 622 in 2021 , 667 in 2022, 712 in 2023, and so on. The plant cannot produce more than 612 prototype chips annually. To meet future demand, A 1 Chips must either modernize the plant or replace it. The old equipment is fully depreciated and can be sold for $4,700,000 if the plant is replaced. If the plant is modernized, the costs to modemize it are to be capitalized and depreciated over the useful life of the modernized plant. The old equipment is retained as part of the "modernize" alternative. Data table The following data on the two options are available: A - 1 Chips uses straight-line depreciation, assuming zero terminal disposal value. For simplicity, we assume no change in prices or costs in future years. The investment will be made at the beginning of 2021, and all transactions thereafter occur on the last day of the year. A - 1 Chips' required rate of return is 12%. There is no difference between the "modernize" and "replace" alternatives in terms of required working capital. A-1 Chips pays a 45% tax rate on all income. Proceeds from sales of equipment above book value are taxed at the same 45% rate. Requirements 1 and 2 Caicidate the ahier-tax cash inflows and outflows of the "modernize" and replace" atematives over the 2021 - 20et period and calculate the net present value for each atemasive. Let's begin weh the "modemize" alternative, Start by computing the present value or the affer tax cash flows from operations, nen cavculate the present value of the after-tax cash savings tom depreciation and the termiral dinposal value, and finally, deterinine the tolal net present value (NPV) of the investmert for the "modence" alternative. (Round intermedlary calciationa and your finar arswers to the nearest whole dotar. Use a minus sign or parentwies for a nepalfe present value of nel casti flows.)